Tuesday, February 09, 2021

Could Twitter’s share price put it ahead of the social media competition?

تم إعداد هذا المنشور من قبل سنشري للاستشارات

Twitter’s [TWTR] share price got off to a rough start in 2020 as the March market sell-off pushed the stock to its lowest value since 2017 — it closed at $22 on 18 March, down 31.4% year-to-date.

However, and despite a few bumps along the way, Twitter’s share price has soared since then, and on 18 December the stock closed at $55.87. This marked 74.3% growth year-to-date and was the stock’s best close since the months directly following its market debut in November 2013. Recently it has climbed even higher, closing at $56.78 on 5 February.

Looking more closely at Twitter’s share price performance during its fourth quarter to 1 January, the stock managed to grow 16% — despite a significant tumble following its third-quarter earnings report on 29 October.

As the social media giant prepares to release its Q4 earnings, due 9 February, how will Twitter’s share price react to the news?

Twitter outpaces the competition

When Twitter announced its Q3 results, it posted diluted earnings per share of $0.04. This not only missed the Zacks Equity Research consensus estimate of $0.06 by 33.3%, but it also marked a decline of 20% year-over-year.

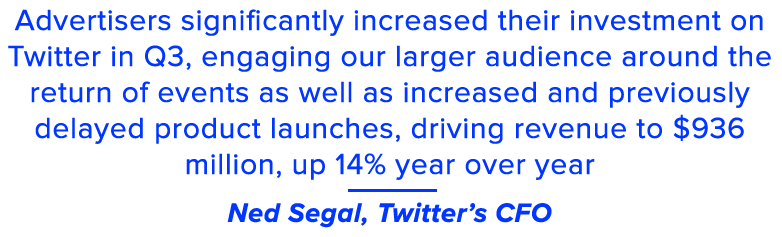

On the other hand, revenues increased 14% year-over-year to total $936m — beating the Zacks consensus estimate of $765.3m by 18.2%.

The better-than-expected revenue was attributed to an increase in advertising revenue for the quarter. Zacks predicted it would have declined 10% year-over-year to $632m, but it actually increased 15% to $808m — a surprise of 27.9% — which amounts to 86% of Twitter’s total revenue for Q3.

“Advertisers significantly increased their investment on Twitter in Q3, engaging our larger audience around the return of events as well as increased and previously delayed product launches, driving revenue to $936 million, up 14% year over year,” said Ned Segal, Twitter’s CFO.

Following the report, Twitter’s share price tumbled 24.7% over a two-day trading period to close at $39.47 on 2 November. Although Twitter gradually recovered the bulk of its lost value, the stock didn’t manage to top its pre-earnings value until 15 December, when it closed at $52.82.

As a major social media platform, Twitter’s performance is a key marker for thematic ETFs such as the Global X Social Media ETF [SOCL]. With a weighting of 6.80%, Twitter is the fourth largest holding in the fund, behind Snap Inc’s [SNAP] 10.25%, Tencent’s [0700.HK] 9.46% and Facebook’s [FB] 7.18%.

Interestingly, SOCL’s performance outpaced all of the aforementioned stocks bar Snap in 2020. The ETF finished the year up 78.1% year-to-date, while Snap soared 206.6% over the year. On the other hand, Twitter — which lagged behind its competitors for much of 2020 — managed to finish the year up 68.95%, outpacing both Tencent and Facebook.

Looking ahead, Zacks predicts Twitter to post earnings of $0.31 and revenues of $1.19bn in its upcoming report. These figures will represent year-over-year growth of 24% and 17.8% respectively.

Can Twitter keep growing its ad revenue?

Heath Terry, analyst at Goldman Sachs, has told clients that “Twitter is well-positioned to benefit from a significant increase in digital advertising spending,” reports Barron’s.

Terry predicts that Twitter’s advertising revenue will grow 24% year-over-year in 2021, compared with the 9% growth of 2020. Barron’s reports that this sharp increase is a reflection of tech companies’ increased ability to target and measure the effect of online advertising, as well as the sophistication with which platforms like Twitter can use the data.

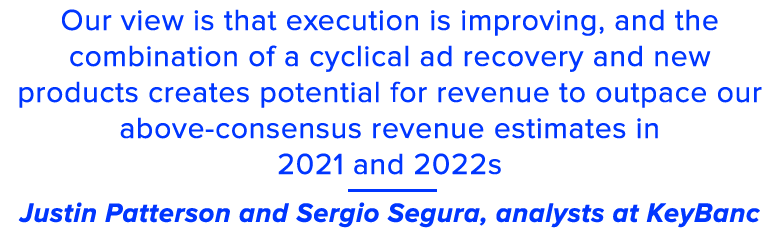

"Our view is that execution is improving, and the combination of a cyclical ad recovery and new products creates potential for revenue to outpace our above-consensus revenue estimates in 2021 and 2022," Justin Patterson and Sergio Segura, analysts at KeyBanc, wrote in a note to clients seen by MarketWatch.

"Under a more bullish scenario, we think Twitter could attain 2022 revenue of $5.7bn (around 10% above consensus)," said the analysts.

Source: This content has been produced by Opto trading intelligence for Century Financial and was originally published on cmcmarkets.com/en-gb/opto

Disclaimer: Past performance is not a reliable indicator of future results.

The material (whether or not it states any opinions) is for general information purposes only and does not take into account your personal circumstances or objectives. Nothing in this material is (or should be considered to be) financial, investment or other advice on which reliance should be placed. No opinion given in the material constitutes a recommendation by Century Financial or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person.

Century Financial does not endorse or offer opinion on the trading strategies used by the author. Their trading strategies do not guarantee any return and Century Financial shall not be held responsible for any loss that you may incur, either directly or indirectly, arising from any investment based on any information contained herein.

تنظمها هيئة الأوراق المالية والسلع

سنشري للاستشارات المالي ش.ذ.م.م

تصل إلينا:

-

دبي

الطابق رقم 6, مبنى رقم 4, ساحة إعمار دبي

وسط مدينة دبي، ص.ب: 65777،

دبي، الإمارات العربية المتحدة -

Abu Dhabi

27th Floor, Office 2701,

Shining Towers, Abu Dhabi, UAE - +971 (4) 356 2800

- info@century.ae

Century Financial is the presenting sponsor of

ينطوي التداول في المنتجات المالية على مخاطر كبيرة. فالاعتماد على المشتقات المالية المتاحة للتداول خارح البورصة، مثل عقود الفروقات وتداول العملات الأجنبية (الفوركس) الفوري، قد يتسبب في خسائر تتجاوز قيمة الإيداعات الأولية، مما يجعلها غير ملائمة لجميع المستثمرين. فهذه الأدوات المالية المعقدة لا تمنح ملكية مباشرة للأصول الأساسية. لذا، ينبغي للمستثمرين الاحتراز عند تحديد أهدافهم الاستثمارية ومراعاة مستوى المخاطرة المتوقَع، واللجوء إلى الاستشارة المهنية المتخصصة عند الضرورة.

سنشري للإستشارات والتحليل المالي ش.ذ.م.م (الشركة)، شركة مرخّصة ومنظمة من هيئة الأوراق المالية والسلع في دولة الإمارات العربية المتحدة، بموجب الترخيص رقم (20200000028) و(301044) لتولي أعمال الوساطة في الأسواق الدولية، وتداول المشتقات المالية والعملات المتاحة للتداول خارج البورصة في سوق التداول الفوري، بالإضافة إلى تقديم الخدمات الاستشارية والترويجية. تأسست الشركة بموجب قوانين دولة الإمارات العربية المتحدة، وهي مسجلة لدى دائرة التنمية الاقتصادية بدبي (رقم: 768189)، حيث يقع مكتبها المسجّل في 601، الطابق السادس، المبنى رقم 4، ميدان إعمار، وسط مدينة دبي، دولة الإمارات العربية المتحدة، ص.ب. 65777.

لا يُعرَض محتوى هذا الموقع الإلكتروني إلا لأغراض تعريفية تثقيفية بحتة، فلا يمثل عرضًا ولا توصيةً ولا دعوةً لشراء أو بيع أي أوراق مالية أو منتجات مالية.

لا تنوي الشركة استخدام أو توزيع منتجاتها وخدماتها في أي ولاية قضائية حيث يُشكِّل هذا الاستخدام أو التوزيع انتهاكًا للقوانين المحلية أو اللوائح التنظيمية.