Tuesday, August 11, 2020

Can Barclays Share Price Rely on Strong Trading Profits?

By Century Financial in 'Brainy Bull'

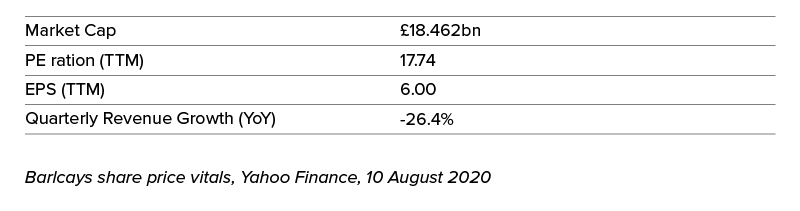

Barclays’ [BARC] share price has put it among the biggest losers of banking so far in 2020. The stock had opened the year at 180.08p but as of 7 August trades at just 104.60p.

As coronavirus fears began to take hold in March, Barclays’ share price fell to a low of 80.24p on 3 April before recovering to 131.80p on 8 June. However, the recovery was short-lived as it fell to 100.56p on 31 July.

Barclay’s share price then climbed 4% over the first seven days of August but has struggled to navigate record low-interest rates blasting margins as well as economic fears over Brexit and the COVID-19 pandemic.

Amid these headwinds, Barclays Corporate and Investment Bank has been a bright spot with income up 31% year-over-year at £6.9bn for the first half of 2020.

Why then has Edward Bramson, founder of Sherborne, revived his activist campaign against the division?

Investment bank woes, despite increased trading

The UK bank’s earnings results for the first half of 2020 laid bare some of those headwinds when it posted a 66% drop in profits to £695m.

Barclays also set aside £3.7bn to cover anticipated bad loans from the pandemic, as businesses and individuals struggle to keep up debt repayments.

It wasn’t all bad news though. Barclays’ trading division posted a 63% hike in trading revenues to £4.56bn, as an increased number of traders looked to make money in the pandemic driven volatility.

Despite the strong performance, Bramson wrote a letter to shareholders on 6 August requesting the bank slim down its investment arm by 24% to boost profits, according to the Financial Times.

Bramson’s Sherborne Investors Management, which holds a 5.9% stake in Barclays, has long seen the investment bank as being dilutive to Barclays’ shareholder returns.

Bramson argues that the trading surge in the first half of the year will not continue. “In the real world, investors do not care very much about the trading business,” Bramson wrote.

Jes Staley, Barclays chief executive, has paid little attention to critics like Bramson instead deciding to expand rather than reduce the size of the investment unit over recent years.

Richard Buxton, a fund manager at Merian Global Investors, believes that Staley’s hybrid model of having investment banking as well as commercial and retail on the cards has proved itself effective at “offsetting tougher times elsewhere”.

However, Staley could still buckle. Despite return on equity in the investment division reaching 9.6% in the second quarter that compares badly to the likes of Goldman Sachs or Credit Suisse that generated returns of 17% and more, according to analysis by eFinancial.

Increased resilience, but for how long?

Judging by MarketScreener’s analysis of Barclays’ share price, the revived investment bank debacle will have very little impact on the stock. Analysts have a consensus outperform rating on the Barclays stock with an average target price of 141.28p.

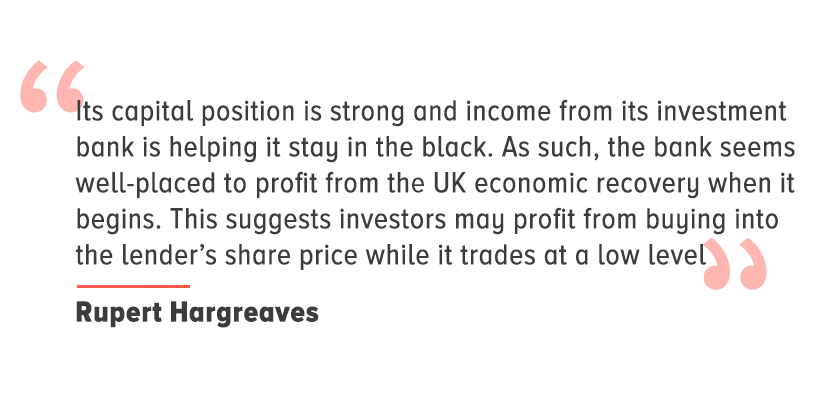

Defaults from the pandemic could weigh on the profits of lenders such as Barclays for years to come. Rupert Hargreaves wrote in The Motley Fool. However, its trading division has helped it sidestep the worse of these losses.

“If the pandemic lasts into 2021, it may be forced to take even more loss provisions impacting the share price,” Hargreaves wrote.

“Still, it should be able to cope. Its capital position is strong, and income from its investment bank is helping it stay in the black. As such, the bank seems well-placed to profit from the UK economic recovery when it begins. This suggests investors may profit from buying into the lender’s share price while it trades at a low level.”

Robert Noble, an analyst at Deutsche Bank, is targeting a price more towards the lower end at 135p.

“At first glance UK banks screen as value, but on a relative basis not materially so — and significant risks remain,” he said, according to Interactive Investor.

The group is likely to face more headwinds in the second half of the year, as government support measures for the economy such as furloughing come to an end and the economic reality begins to bite.

Its investment arm will provide its share price with some resilience but for how much longer is unclear.

Source: This content has been produced by Opto trading intelligence for Century Financial and was originally published on cmcmarkets.com/en-gb/opto

Disclaimer: Past performance is not a reliable indicator of future results.

The material (whether or not it states any opinions) is for general information purposes only and does not take into account your personal circumstances or objectives. Nothing in this material is (or should be considered to be) financial, investment or other advice on which reliance should be placed. No opinion given in the material constitutes a recommendation by Century Financial or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person.

Century Financial does not endorse or offer opinion on the trading strategies used by the author. Their trading strategies do not guarantee any return and Century Financial shall not be held responsible for any loss that you may incur, either directly or indirectly, arising from any investment based on any information contained herein.

Regulated by SCA

Century Financial Consultancy LLC

Reach us:

-

Dubai

6th Floor, Emaar Square Building 4,

Downtown, Dubai, P.O. Box 65777,

Dubai, United Arab Emirates -

Abu Dhabi

27th Floor, Office 2701,

Shining Towers, Abu Dhabi, UAE - +971 (4) 356 2800

- info@century.ae

Disclaimer: Trading in financial products carries substantial risk. Leveraged over-the-counter (OTC) derivatives, such as Contracts for Difference (CFDs) and spot forex, may result in losses exceeding initial deposits and may not be suitable for all investors. These complex instruments do not confer ownership of the underlying assets. Investors should carefully consider their investment objectives and risk appetite, and seek independent professional advice if necessary.

Century Financial Consultancy LLC (CFC) is licensed and regulated by the Securities and Commodities Authority (SCA) of the UAE under license numbers 20200000028 and 301044 to carry out the activities of Trading Broker in international markets, Trading Broker of OTC derivatives and currencies in the spot market, Introduction, Financial Consultations, and Promotion. CFC is incorporated under UAE law, registered with the Dubai Economic Department (No. 768189), with its office at 601, Level 6, Building No. 4, Emaar Square, Downtown Dubai, UAE, PO Box 65777.

The content on this website is provided solely for informational and educational purposes and does not constitute an offer, recommendation, or solicitation to buy or sell any securities or financial products.

Products and services offered by CFC are not intended for use in any jurisdiction where such use or distribution would breach local laws or regulatory requirements.

Alert: Fraudulent Activity Notice

Century Financial Consultancy LLC (“Century”) has become aware of fraudulent individuals and entities impersonating our firm through unofficial websites, social media channels, and messaging applications such as Telegram, WhatsApp, and Discord.

Please be advised:

- Century does not manage investments on behalf of clients.

- Century does not solicit funds or guarantee investment returns.

- Century does not accept or make payments in cash, cryptocurrency, or digital assets.

- We do not conduct business via social media or messaging platforms.

Our only official website is www.century.ae, and all communication is conducted exclusively through verified channels.

We strongly urge the public to remain vigilant, verify the authenticity of any communication claiming to be from Century, and report any suspicious activity. Century disclaims any responsibility for losses arising from dealings with unauthorised or fraudulent parties.