Tuesday, May 12, 2020

Amazon’s share price is booming – is the stock a safe bet post-Coronavirus?

By Century Financial in 'Brainy Bull'

Amazon’s [AMZN] share price hit an all-time high after Q1 saw sales increase by 26% year-on-year in Q1. What is it doing to future-proof its business, and will its stock keep soaring after lockdown?

At a time when physical shops are shut and people are staying at home, Amazon [AMZN] has been kept busy with a surge of orders. But is Amazon’s share price a safe bet for investors?

Back in April, investment bank Cowen took note of the company’s sales bonanza. In a note to clients, it said: “Amazon has seen enormous increase in demand as shoppers are forced to stay home, essentially creating an extended Prime Day/Black Friday type of situation.”

Amazon’s share price responded accordingly, rising 28% throughout the course of April. This comes on the back of Amazon’ share price reaching its 52-week low of $1,626.03 during the market sell-off.

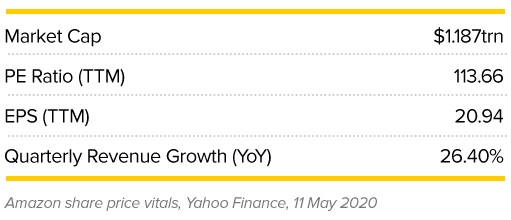

Share price performance was underlined by Amazon’s earnings haul. The early results of the pandemic sales boom were revealed in Amazon’s Q1 2020 earnings call on 30 April. The company confirmed quarterly revenue of $75.45bn, which marked a 26% year-over-year increase on Q1 2019’s $59.7bn. It also surpassed the Refinitiv consensus estimate of $73.61bn.

Amazon cloud’s segment, which is a key part of its business, boasted revenue of $10.2bn, passing the eleven-digit mark for the first time — it was a 32.5% year-over-year increase on Q1 2019’s cloud revenue. To put the cloud revenue into context, Google’s parent company Alphabet [GOOGL] posted $2.78bn in Google Cloud revenue for its first quarter of 2020, a 52% year-over-year increase. But is this extended capacity conducive to long-term share price gains?

Will increased spending drag Amazon’s share price down?

The downside is that Amazon posted an earnings miss. Analysts had been expecting earnings per share to be $6.25, but the actual EPS figure came in almost 20% lower at $5.01. This was also 29% lower than Q1 2019’s EPS of $7.09. Though largely positive, Amazon’s earnings have been up and down over the last few years. Data from Zacks shows that, since the start of fiscal 2017, the company has now posted four EPS misses and nine beats.

Operating profit, meanwhile, was down 9% year-over-year to $4bn. Amazon now predicts that in Q2 it will report anything between an operating loss of $1.5bn to a profit of $1.5bn. The wide range is due to the financial uncertainty that Covid-19 has created, and the fact that the company is committed to reinvesting most, if not all, of the profit, made. So, what course of action does Jeff Bezos suggest Amazon’s share price investors take?

“If you’re a share owner in Amazon, you may want to take a seat,” said Bezos during the earning call. “Under normal circumstances, in this coming Q2, we’d expect to make some $4bn or more in operating profit. But these aren’t normal circumstances. Instead, we expect to spend the entirety of that $4bn, and perhaps a bit more, on COVID-related expenses getting products to customers and keeping employees safe.”

The company has already had to hire an additional 175,000 staff to cope with the increased demand in deliveries, develop its own testing system for the virus, introduce personal protective equipment and enhance the cleaning of its warehouses and facilities.

Future-proofing: Can Amazon increase customer acquisition?

In the short-term, investors may be concerned by the potential for a huge operational loss, but it’s arguably a move the company needs to make in order to future-proof its business and take advantage of a challenging environment. These costs may be high, but they are temporary.

Oppenheimer analyst Jason Helfstein said: “[Return on investment] of this $4bn will become apparent in Q4 and 2021 if Amazon is able to accelerate consumer adoption of its services.”

In a note to clients, RBC Capital Markets’ equity analyst Mark Mahaney said he viewed the company as “a structural winner”, adding that “the COVID crisis accelerates the shift to online retail and businesses [are deepening] their transformation to digital, benefiting Amazon Web Services.”

Looking beyond the second quarter, Amazon is primed to take advantage of the situation. RBC recently released its fifth annual user survey on online grocery trends. As part of a snapshot of the report, Mahaney said that before lockdowns and social distancing came into force more than half of consumers bought groceries online. Many are more willing to continue doing so because they realise it’s convenient.

“If Amazon can optimise the customer experience — a very challenging proposition in this environment — it can dramatically benefit, with groceries becoming a larger portion of its revenue in a few years,” he wrote.

On the day of the earnings release on 30 April, Amazon’s share price reached an all-time closing high of $2,474, but consequently fell around 5% in after-hours trading. It has since dropped back further. As of 8 May, the share price closed at $2,379.61.

In the last 30 days, the majority of Wall Street analysts have raised their share price targets, with the consensus among 48 of them currently sitting at $2,562.42, according to MarketBeat. Of the ratings issued, an overwhelming majority - 44 - have assigned a buy rating, three a hold, and one a sell.

Source: This content has been produced by Opto trading intelligence for Century Financial and was originally published on cmcmarkets.com/en-gb/opto

Disclaimer: Past performance is not a reliable indicator of future results.

The material (whether or not it states any opinions) is for general information purposes only and does not take into account your personal circumstances or objectives. Nothing in this material is (or should be considered to be) financial, investment or other advice on which reliance should be placed. No opinion given in the material constitutes a recommendation by Century Financial or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person.

Century Financial does not endorse or offer opinion on the trading strategies used by the author. Their trading strategies do not guarantee any return and Century Financial shall not be held responsible for any loss that you may incur, either directly or indirectly, arising from any investment based on any information contained herein.

Regulated by CMA

Century Financial Consultancy LLC

.png)

.png)

.png)

.png)

.png)

Reach us:

-

Dubai

6th Floor, Emaar Square Building 4,

Downtown, Dubai, P.O. Box 65777,

Dubai, United Arab Emirates -

Abu Dhabi

27th Floor, Office 2701,

Shining Towers, Abu Dhabi, UAE -

Sharjah

29th Floor, Office 2905,

The Business Tower, Sharjah, UAE - +971 (4) 356 2800

- info@century.ae

Disclaimer: Trading in financial products carries substantial risk. Leveraged over-the-counter (OTC) derivatives, such as Contracts for Difference (CFDs) and spot forex, may result in losses exceeding initial deposits and may not be suitable for all investors. These complex instruments do not confer ownership of the underlying assets. Investors should carefully consider their investment objectives and risk appetite, and seek independent professional advice if necessary.

Century Financial Consultancy LLC (CFC) is licensed and regulated by the Capital Market Authority (CMA) of the UAE under license numbers 20200000028 and 301044 to carry out the activities of Financial Products dealer, Trading Broker in international markets, Trading Broker of OTC derivatives and currencies in the spot market, Introduction, Financial Consultations, and Promotion. CFC is incorporated under UAE law, registered with the Dubai Economic Department (No. 768189), with its office at 601, Level 6, Building No. 4, Emaar Square, Downtown Dubai, UAE, PO Box 65777.

The content on this website is provided solely for informational and educational purposes and does not constitute an offer, recommendation, or solicitation to buy or sell any securities or financial products.

Products and services offered by CFC are not intended for use in any jurisdiction where such use or distribution would breach local laws or regulatory requirements.

⚠️ Alert: Fraudulent Activity Notice

Century Financial Consultancy LLC (“Century”) has become aware of fraudulent individuals and entities impersonating our firm through unofficial websites, social media channels, and messaging applications such as Telegram, WhatsApp, and Discord.

Please be advised:

- Century does not manage investments on behalf of clients.

- Century does not solicit funds or guarantee investment returns.

- Century does not accept or make payments in cash, cryptocurrency, or digital assets.

- We do not conduct business via social media or messaging platforms.

Our only official website is www.century.ae, and all communication is conducted exclusively through verified channels.

We strongly urge the public to remain vigilant, verify the authenticity of any communication claiming to be from Century, and report any suspicious activity. Century disclaims any responsibility for losses arising from dealings with unauthorised or fraudulent parties.