Wednesday, July 01, 2020

Can IAG’s share price get off the ground?

By Century Financial in 'Brainy Bull'

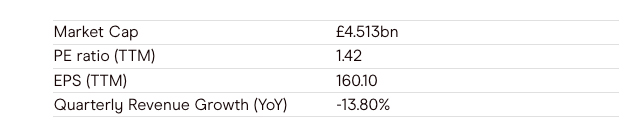

International Airlines Group's [IAG] share price is down 63.8% so far in 2020 (through 29 June’s close). The stock closed 68.2% off its all-time high of 726.60p, which it reached in June 2018.

Unsurprisingly, IAG’s share price plummeted in February as the coronavirus pandemic took hold. Like other big names in the airline industry, the share price bottomed out in the first half of May, before seeming to make an impressive recovery. From mid-May, IAG’s share price gained 97% in just over three weeks, a rally that was in-line with much of the wider airline industry. Unfortunately, the recovery was short-lived.

So, as the industry’s value takes a new nosedive, what is the outlook for IAG’s share price?

Time to buy the dip?

Following IAG’s impressive May rally, it became clear in early June that investors were getting ahead of themselves, and share prices across the airline industry were being carried by momentum more than facts on the ground. IAG’s share price dropped 33.1% between 8 June and 25 June.

Airlines have been amongst the hardest hit by the pandemic, which has grounded flights globally. IAG’s share price is not the only one to have plummeted so far this year, and Bloomberg suggest that the industry could collectively lose an eye-watering $84bn in 2020.

With the recent rally and subsequent pullback of IAG’s share price, many investors will be wondering whether now is the time to buy the dip.

It was recently reported that IAG has begun working with Goldman Sachs and Morgan Stanley in order to assess its business plan going forward, with the prospect of a repositioning of the group following the pandemic.

This news comes as it was revealed that British Airways is set to cut 30% of its workforce, amounting to 12,000 jobs. In the immediate future, it appears that securing long-term credit will be IAG’s next step. The firm has already raised large amounts to protect itself during the pandemic, but this is believed to be short-term debt that will need to be refinanced.

Considering the current situation, it seems that another large-scale rally with sustained gains in 2020 may be unlikely, even if there is some room for IAG’s share price to increase. The group is facing a range of serious challenges, from raising credit to low sales and the prospect of a second coronavirus wave in Europe threatening even more grounded flights.

Confirming the issues facing the group, CEO Willie Walsh recently acknowledged the need for restructuring. “We do not expect passenger demand to recover to the level of 2019 before 2023 at the earliest,” he said during the company’s quarterly results announcement. “Balance sheets are going to be very different when we come out of this. Structural reform is going to be required on an industry basis and not just on an individual airline basis.”

Survival of the fittest

There is, however, little doubt that the group will survive, and IAG’s share price will recover. At the end of April, the group had access to $12.4bn in reserves. This war chest puts the company in a “very strong liquidity position” that will enable it to “outlast many peers” in the event of an extended grounding and downturn, Daniel Roeska, an analyst at Sanford C. Bernstein, wrote in a note seen by Bloomberg.

However, it is likely that the IAG that emerges on the other side of this outbreak will have significantly downsized. The company already plans to half its normal orders of new planes in the next three years, taking delivery of just 75 of the planned 143.

Despite this, analysts are bullish on IAG’s share price. The consensus among 18 analysts polled by MarketBeat is to buy the stock, a rating given by 14, while 4 rate it a hold. An average 12-month price target of $427.81 would represent an 85.5% upside on the current price (as of 29 June’s close).

While there is room for IAG’s share price to move higher if sales pick up again in 2021, it is asking a lot to expect a slimmed-down version of the group to match its previous highs. IAG will have to provide investors with some convincing figures if confidence is to be fully restored.

Source: This content has been produced by Opto trading intelligence for Century Financial and was originally published on cmcmarkets.com/en-gb/opto

Disclaimer: Past performance is not a reliable indicator of future results.

The material (whether or not it states any opinions) is for general information purposes only and does not take into account your personal circumstances or objectives. Nothing in this material is (or should be considered to be) financial, investment or other advice on which reliance should be placed. No opinion given in the material constitutes a recommendation by Century Financial or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person.

Century Financial does not endorse or offer opinion on the trading strategies used by the author. Their trading strategies do not guarantee any return and Century Financial shall not be held responsible for any loss that you may incur, either directly or indirectly, arising from any investment based on any information contained herein.

Regulated by CMA

Century Financial Consultancy LLC

.png)

.png)

.png)

.png)

.png)

Reach us:

-

Dubai

6th Floor, Emaar Square Building 4,

Downtown, Dubai, P.O. Box 65777,

Dubai, United Arab Emirates -

Abu Dhabi

27th Floor, Office 2701,

Shining Towers, Abu Dhabi, UAE -

Sharjah

29th Floor, Office 2905,

The Business Tower, Sharjah, UAE - +971 (4) 356 2800

- info@century.ae

Disclaimer: Trading in financial products carries substantial risk. Leveraged over-the-counter (OTC) derivatives, such as Contracts for Difference (CFDs) and spot forex, may result in losses exceeding initial deposits and may not be suitable for all investors. These complex instruments do not confer ownership of the underlying assets. Investors should carefully consider their investment objectives and risk appetite, and seek independent professional advice if necessary.

Century Financial Consultancy LLC (CFC) is licensed and regulated by the Capital Market Authority (CMA) of the UAE under license numbers 20200000028 and 301044 to carry out the activities of Financial Products dealer, Trading Broker in international markets, Trading Broker of OTC derivatives and currencies in the spot market, Introduction, Financial Consultations, and Promotion. CFC is incorporated under UAE law, registered with the Dubai Economic Department (No. 768189), with its office at 601, Level 6, Building No. 4, Emaar Square, Downtown Dubai, UAE, PO Box 65777.

The content on this website is provided solely for informational and educational purposes and does not constitute an offer, recommendation, or solicitation to buy or sell any securities or financial products.

Products and services offered by CFC are not intended for use in any jurisdiction where such use or distribution would breach local laws or regulatory requirements.

⚠️ Alert: Fraudulent Activity Notice

Century Financial Consultancy LLC (“Century”) has become aware of fraudulent individuals and entities impersonating our firm through unofficial websites, social media channels, and messaging applications such as Telegram, WhatsApp, and Discord.

Please be advised:

- Century does not manage investments on behalf of clients.

- Century does not solicit funds or guarantee investment returns.

- Century does not accept or make payments in cash, cryptocurrency, or digital assets.

- We do not conduct business via social media or messaging platforms.

Our only official website is www.century.ae, and all communication is conducted exclusively through verified channels.

We strongly urge the public to remain vigilant, verify the authenticity of any communication claiming to be from Century, and report any suspicious activity. Century disclaims any responsibility for losses arising from dealings with unauthorised or fraudulent parties.