Thursday, January 21, 2021

Is the Semiconductor Affecting Intel’s Share Price

By Century Financial in 'Brainy Bull'

Intel Corporation’s [INTC] chips were down in 2020, mainly due to manufacturing issues. Will Q4 earnings, due 21 January, give an indication as to whether Intel’s share price can turn a corner this year?

Intel’s share price dropped 14.7% last year after closing at $49.82 on 31 December 2020. It had peaked at a 52-week high of $69.29 during intraday trading on 24 January 2020 and fell to a 52-week low of $43.61 on 30 October.

By contrast, rival chipmakers Nvidia [NVDA] and Taiwan Semiconductor Manufacturing Co (TSMC) [TSM] gained 122% and 92% respectively in 2020.

However, Intel’s share price performance since the start of this year suggests things could be on the up. It had gained 16.4% year-to-date as of close on 19 January.

Production issues

Intel’s share price was dragged down partly because the company was forced to delay production of its next-generation 7nm (nanometre) chips due to manufacturing issues. Intel is one of the only chipmakers to rely predominantly on in-house manufacturing.

The most recent quarterly report indicated that the company was considering transferring much of its manufacturing to TSMC.

Intel’s data-centre business showed signs of weakness in the Q3 report — revenue was $5.9bn in Q3 2020, down almost 8% from the $6.4bn reported in Q3 2019, and down nearly 17% on the previous quarter’s data-centre revenue of $7.1bn.

The Client Computing Group (CCG), which includes sales from PC chips, continued to be boosted by people needing computers to work and study from home. Revenue for the segment grew 1% year-over-year from $9.7bn in Q3 2019 to $9.8bn. It was up 3.2% on the $9.5bn revenue reported in Q2 2020.

Total revenue for the three months to the end of September was $18.33bn, down 4.5% from the $19.19bn reported in the year-ago quarter — this marked the firm’s first year-over-year decline since Q2 2019. Earnings per share were $1.11. These figures were more or less in line with what analysts polled by Refinitv had been expecting, according to CNBC.

Despite meeting expectations, Intel’s share price fell by as much as 10% during after-hours trading as investors contemplated what impact a continuing decline in data-centre revenue might have on future growth.

With regard to Q4 2020 earnings, Intel has issued guidance of $17.4bn revenue, which would be a 13.9% fall year-over-year; earnings per share are forecast to be $1.06. The latest analyst estimates, according to Zacks Equity Research, are revenue in the range of $17.4bn and $17.66bn, and earnings per share between $1.09 and $1.11.

Looking ahead

The movement Intel’s share price will make following the upcoming earnings report will not only depend on whether it beats its forecast and expectations. Investors will also be looking to see if the company gives any indication as to the future performance of its data centre group, as well as any updates on the manufacturing of its 7nm chips.

A Bloombergreport earlier this month confirmed that Intel was considering outsourcing production to TSMC, supporting comments Intel CEO Bob Swan made last year. The publication also named Samsung [005930] as another potential manufacturing partner. Other recent reports suggest an outsourcing partnership may have already begun.

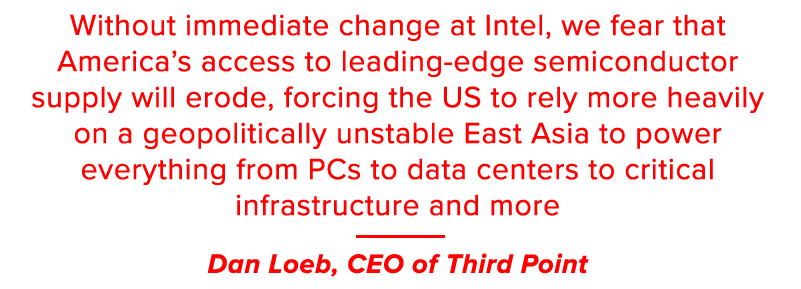

At the end of December, Dan Loeb, CEO of Third Point, wrote to Intel’s executive team, asking them to consider splitting its chip manufacturing business from its chip design and development business. Loeb also suggested that the company consider strategic alternatives. Intel lags behind its rivals in terms of cutting-edge chip manufacturing technology.

“Without immediate change at Intel, we fear that America’s access to leading-edge semiconductor supply will erode, forcing the US to rely more heavily on a geopolitically unstable East Asia to power everything from PCs to data centers to critical infrastructure and more,” Loeb wrote in a note seen by Barron’s.

On the other hand, Stacy Rasgon, analyst with Bernstein Research, has said that spinning off the chip manufacturing business “doesn’t fix anything”, according to a Reuters news report. Rasgon reiterated a sell rating and price target of $40.

In total, Intel currently has 43 Wall Street ratings, MarketBeatdata shows: 19 buy, 14 hold and 10 sell. The consensus price target is $60.47, which would be a 4.3% increase on its current price (through 19 January’s close).

Source: This content has been produced by Opto trading intelligence for Century Financial and was originally published on cmcmarkets.com/en-gb/opto

Disclaimer: Past performance is not a reliable indicator of future results.

The material (whether or not it states any opinions) is for general information purposes only and does not take into account your personal circumstances or objectives. Nothing in this material is (or should be considered to be) financial, investment or other advice on which reliance should be placed. No opinion given in the material constitutes a recommendation by Century Financial or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person.

Century Financial does not endorse or offer opinion on the trading strategies used by the author. Their trading strategies do not guarantee any return and Century Financial shall not be held responsible for any loss that you may incur, either directly or indirectly, arising from any investment based on any information contained herein.

Regulated by CMA

Century Financial Consultancy LLC

.png)

.png)

.png)

.png)

.png)

Reach us:

-

Dubai

6th Floor, Emaar Square Building 4,

Downtown, Dubai, P.O. Box 65777,

Dubai, United Arab Emirates -

Abu Dhabi

27th Floor, Office 2701,

Shining Towers, Abu Dhabi, UAE -

Sharjah

29th Floor, Office 2905,

The Business Tower, Sharjah, UAE - +971 (4) 356 2800

- info@century.ae

Disclaimer: Trading in financial products carries substantial risk. Leveraged over-the-counter (OTC) derivatives, such as Contracts for Difference (CFDs) and spot forex, may result in losses exceeding initial deposits and may not be suitable for all investors. These complex instruments do not confer ownership of the underlying assets. Investors should carefully consider their investment objectives and risk appetite, and seek independent professional advice if necessary.

Century Financial Consultancy LLC (CFC) is licensed and regulated by the Capital Market Authority (CMA) of the UAE under license numbers 20200000028 and 301044 to carry out the activities of Financial Products dealer, Trading Broker in international markets, Trading Broker of OTC derivatives and currencies in the spot market, Introduction, Financial Consultations, and Promotion. CFC is incorporated under UAE law, registered with the Dubai Economic Department (No. 768189), with its office at 601, Level 6, Building No. 4, Emaar Square, Downtown Dubai, UAE, PO Box 65777.

The content on this website is provided solely for informational and educational purposes and does not constitute an offer, recommendation, or solicitation to buy or sell any securities or financial products.

Products and services offered by CFC are not intended for use in any jurisdiction where such use or distribution would breach local laws or regulatory requirements.

⚠️ Alert: Fraudulent Activity Notice

Century Financial Consultancy LLC (“Century”) has become aware of fraudulent individuals and entities impersonating our firm through unofficial websites, social media channels, and messaging applications such as Telegram, WhatsApp, and Discord.

Please be advised:

- Century does not manage investments on behalf of clients.

- Century does not solicit funds or guarantee investment returns.

- Century does not accept or make payments in cash, cryptocurrency, or digital assets.

- We do not conduct business via social media or messaging platforms.

Our only official website is www.century.ae, and all communication is conducted exclusively through verified channels.

We strongly urge the public to remain vigilant, verify the authenticity of any communication claiming to be from Century, and report any suspicious activity. Century disclaims any responsibility for losses arising from dealings with unauthorised or fraudulent parties.