Tuesday, August 04, 2020

Is Beyond Meat’s share price unsustainable?

By Century Financial in 'Brainy Bull'

Judging by Beyond Meat’s [BYND] share price, it’s been a big winner during the coronavirus pandemic. In its second-quarter Beyond Meat’s share price rose an astronomical 102%.

As slaughterhouses shut and processing facilities ground to a halt, meat lovers turned to plant-based substitutes to satisfy their cravings.

Although Beyond Meat’s share price of $125.90 on 31 July was some way off the 52-week high set last summer, it’s also 161.3% of the 52-week low it experienced during the March sell-off.

However, despite the recent bullish performance, it’s possible that the stock has bitten off more than it can chew and a number of analysts appear to have lost their appetite for the share price.

What will happen to Beyond Meat’s share price when it releases its Q2 earnings reports on 4 August?

Will growth slow in Q2?

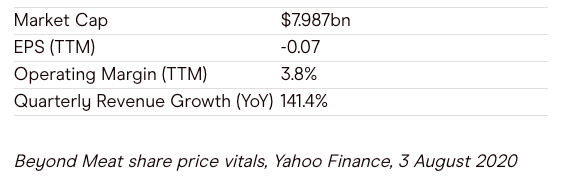

In the first quarter of 2020, Beyond Meat reported that revenue was up 141% at $97.07m. Domestic retail sales were up 156% at $49.9m, with food service sales up 156% at $22.6m. As for international revenue, global retail sales were $5.9m, while global food service revenue was up 57% at $18.6m.

According to Zacks Equity Research, the consensus estimate for revenue for Q2 is $97m, which would mark a 44% increase year-over-year. However, earnings are expected to drop 300% year-over-year to $0.02 per share. Beyond Meat itself hasn’t issued any guidance.

For the second quarter of the fiscal year, Bernstein analyst Alexia Howard expects the company to post revenue of around $102m, which would be a 52% year-over-year increase. This sounds impressive, but would be much lower than Q1 2020’s gains.

Beyond Q2 2020, food service revenue is unlikely to climb significantly while restaurants are either closed or operating with social distancing measures in place.

Although the company has been pushing ahead with its international expansion, going by Q1 2020’s earnings, international sales account for around a quarter of total revenue.

Furthermore, while the company signed a deal with Yum China Holdings [YUMC] in June to introduce its burgers into select branches of KFC, Pizza Hut and Taco Bell, it’s only a limited run. There’s no guarantee that its plant-based meat will be added to menus indefinitely.

Closer to home, McDonald’s [MCD] in Canada brought a trial of Beyond Meat’s products to an early end at the start of the quarter in April. Ethan Brown, CEO of Beyond Meat, hopes that it could still lead to a permanent deal, but there has been no update so far.

On top of this, and as a result of eating establishments being shuttered, the company expects gross margin to be lower for the second quarter. Another headwind that it faced during the quarter is the cost of repurposing some of its inventory — originally designated for the food service industry — for retail stock-keeping units.

Analysts lose their appetite

Beyond Meat received a downgrade from Barclays analyst Benjamin Theurer in June. He lowered his rating from overweight to underweight, citing reduced foodservice revenue as a major headwind.

Sales from the food service segment — mainly to restaurants — usually account around half of the company’s total revenue, with the rest coming from retail.

Howard also believes the exposure to the disruption in the food service industry means that there may be little movement for the stock in the short-term.

“This significant slowdown in sales growth could shock some retail investors, who tend to move the stock,” Howard wrote in a note to clients, according to Barron’s, although she did reiterate a market perform rating.

However, Howard underlined her long-term conviction in Beyond Meat’s share price when she raised her price target from $118 to $133.

According to Market Beat data, there are currently 21 Wall Street analysts rating the share price, of which nine rate it a sell, seven a hold and five a buy. The consensus target for Beyond Meat’s share price is $103.84, representing a 17.5% decrease on Friday’s levels.

Source: This content has been produced by Opto trading intelligence for Century Financial and was originally published on cmcmarkets.com/en-gb/opto

Regulated by CMA

Century Financial Consultancy LLC

.png)

.png)

.png)

.png)

.png)

Reach us:

-

Dubai

6th Floor, Emaar Square Building 4,

Downtown, Dubai, P.O. Box 65777,

Dubai, United Arab Emirates -

Abu Dhabi

27th Floor, Office 2701,

Shining Towers, Abu Dhabi, UAE -

Sharjah

29th Floor, Office 2905,

The Business Tower, Sharjah, UAE - +971 (4) 356 2800

- info@century.ae

Disclaimer: Trading in financial products carries substantial risk. Leveraged over-the-counter (OTC) derivatives, such as Contracts for Difference (CFDs) and spot forex, may result in losses exceeding initial deposits and may not be suitable for all investors. These complex instruments do not confer ownership of the underlying assets. Investors should carefully consider their investment objectives and risk appetite, and seek independent professional advice if necessary.

Century Financial Consultancy LLC (CFC) is licensed and regulated by the Capital Market Authority (CMA) of the UAE under license numbers 20200000028 and 301044 to carry out the activities of Financial Products dealer, Trading Broker in international markets, Trading Broker of OTC derivatives and currencies in the spot market, Introduction, Financial Consultations, and Promotion. CFC is incorporated under UAE law, registered with the Dubai Economic Department (No. 768189), with its office at 601, Level 6, Building No. 4, Emaar Square, Downtown Dubai, UAE, PO Box 65777.

The content on this website is provided solely for informational and educational purposes and does not constitute an offer, recommendation, or solicitation to buy or sell any securities or financial products.

Products and services offered by CFC are not intended for use in any jurisdiction where such use or distribution would breach local laws or regulatory requirements.

⚠️ Alert: Fraudulent Activity Notice

Century Financial Consultancy LLC (“Century”) has become aware of fraudulent individuals and entities impersonating our firm through unofficial websites, social media channels, and messaging applications such as Telegram, WhatsApp, and Discord.

Please be advised:

- Century does not manage investments on behalf of clients.

- Century does not solicit funds or guarantee investment returns.

- Century does not accept or make payments in cash, cryptocurrency, or digital assets.

- We do not conduct business via social media or messaging platforms.

Our only official website is www.century.ae, and all communication is conducted exclusively through verified channels.

We strongly urge the public to remain vigilant, verify the authenticity of any communication claiming to be from Century, and report any suspicious activity. Century disclaims any responsibility for losses arising from dealings with unauthorised or fraudulent parties.