Wednesday, May 27, 2020

The shape Barclays’ William Hobbs thinks the recovery will take

By Century Financial in 'Brainy Bull'

William Hobbs, chief investment officer at Barclays states “many economies are experiencing a recession that statistics … weren’t designed to describe”. He points to the unemployment rate as an example, which following the Great Crash in 1929 took 24 months to reach 14%.

“This time it was a matter of months [before the rate hit 14.7% in April]. It is a genuinely extraordinary situation,” Hobbs considers.

However, markets have since been able to rally. The S&P 500, for example, plunged from a high of $3,386 in the middle of February to reach a low of $2,237 on 23 March but has since recovered to $2,948 as of 21 May.

“We actually did suspect that this rally was possible back in the darker days of March and April, and invested accordingly,” Hobbs says. “Markets are forward-looking instruments … and prices always reflect an evolving assessment of a range of probable future outcomes.”

Listen to the full podcast episode here:

Skewing statistics

He explains that in extreme downturns “the range of probabilities becomes much more skewed towards left tail risks.” However, he does note that incredibly forceful intervention did help with market recovery.

One example was the US Federal Reserve, which pumped $2.3trn into the US economy and effectively cut interest rates to zero.

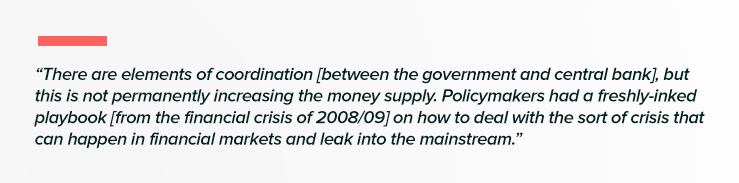

“They are still creating a balance sheet,” Hobbs explains. “There are elements of coordination [between the government and central bank], but this is not permanently increasing the money supply. Policymakers had a freshly-inked playbook [from the financial crisis of 2008/09] on how to deal with the sort of crisis that can happen in financial markets and leak into the mainstream."

He says that the lesson from the last crisis was not to wait., and was impressed by the speed of action that central banks took around the world.

Uncomfortable territory

Hobbs admitted, however, that there are some concerns that the Fed’s actions over the pandemic may have created problems for the future.

“A lot of people are focused on the idea that the Fed has gone down to junk [debt] and included that in its palette of viable securities,” he explains. “It feels uncomfortable territory for the future but if they had not been this aggressive and forceful there [could have been] seriously bleak scenarios.”

He adds that it is also interesting how differently various economies are managing the crisis.

“The US labor market prizes agility so it’s easier to hire and make people redundant, which means unemployment rises much quicker but comes down a lot quicker. [Without a furloughing scheme] will consumers now want to save more of that post-tax earnings for that now very vivid rainy day?”

However, given this “novel situation,” it is hard to predict how tough this recession will be and when it might end.

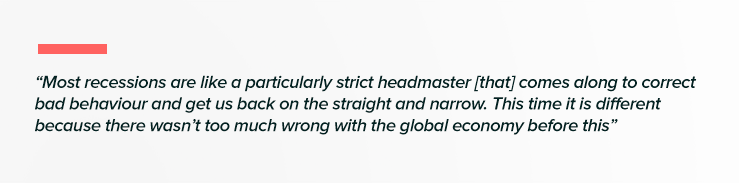

“Most recessions are like a particularly strict headmaster [that] comes along to correct bad behaviour and get us back on the straight and narrow,” Hobbs says. “This time it is different because there wasn’t too much wrong with the global economy before this."

"Prior to the crisis", he explains, "the relatively good health of a number of the major players means that policymakers “deliberately put large chunks of the economy into some kind of induced coma to facilitate fighting the virus.” He says depending on the success of this course of action “the shape of the recovery could look quite different from a big financial crisis or other type of recession.”

Hobbs admits that Barclays is becoming increasingly neutral on risk right now.

“I’m not sure whether that argues for a huge slump in stocks but what it does suggest is that there is a little bit less capacity for markets to absorb new bad news than there was back in March.”

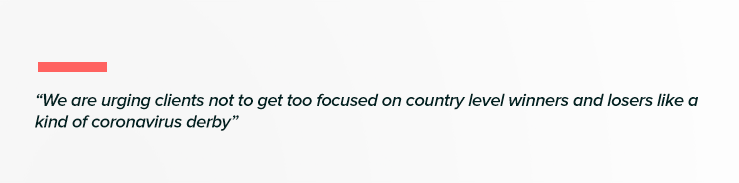

The good news, he adds, has been the US and the tech sector, which have been the “stars of the show so far”, but warns that it is not a foregone conclusion this will continue.

“We are urging clients not to get too focused on country level winners and losers like a kind of coronavirus derby.”

Source: This content has been produced by Opto trading intelligence for Century Financial and was originally published on cmcmarkets.com/en-gb/opto

Disclaimer: Past performance is not a reliable indicator of future results.

The material (whether or not it states any opinions) is for general information purposes only and does not take into account your personal circumstances or objectives. Nothing in this material is (or should be considered to be) financial, investment or other advice on which reliance should be placed. No opinion given in the material constitutes a recommendation by Century Financial or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person.

Century Financial does not endorse or offer opinion on the trading strategies used by the author. Their trading strategies do not guarantee any return and Century Financial shall not be held responsible for any loss that you may incur, either directly or indirectly, arising from any investment based on any information contained herein.

Regulated by CMA

Century Financial Consultancy LLC

.png)

.png)

.png)

.png)

.png)

Reach us:

-

Dubai

6th Floor, Emaar Square Building 4,

Downtown, Dubai, P.O. Box 65777,

Dubai, United Arab Emirates -

Abu Dhabi

27th Floor, Office 2701,

Shining Towers, Abu Dhabi, UAE -

Sharjah

29th Floor, Office 2905,

The Business Tower, Sharjah, UAE - +971 (4) 356 2800

- info@century.ae

Disclaimer: Trading in financial products carries substantial risk. Leveraged over-the-counter (OTC) derivatives, such as Contracts for Difference (CFDs) and spot forex, may result in losses exceeding initial deposits and may not be suitable for all investors. These complex instruments do not confer ownership of the underlying assets. Investors should carefully consider their investment objectives and risk appetite, and seek independent professional advice if necessary.

Century Financial Consultancy LLC (CFC) is licensed and regulated by the Capital Market Authority (CMA) of the UAE under license numbers 20200000028 and 301044 to carry out the activities of Financial Products dealer, Trading Broker in international markets, Trading Broker of OTC derivatives and currencies in the spot market, Introduction, Financial Consultations, and Promotion. CFC is incorporated under UAE law, registered with the Dubai Economic Department (No. 768189), with its office at 601, Level 6, Building No. 4, Emaar Square, Downtown Dubai, UAE, PO Box 65777.

The content on this website is provided solely for informational and educational purposes and does not constitute an offer, recommendation, or solicitation to buy or sell any securities or financial products.

Products and services offered by CFC are not intended for use in any jurisdiction where such use or distribution would breach local laws or regulatory requirements.

⚠️ Alert: Fraudulent Activity Notice

Century Financial Consultancy LLC (“Century”) has become aware of fraudulent individuals and entities impersonating our firm through unofficial websites, social media channels, and messaging applications such as Telegram, WhatsApp, and Discord.

Please be advised:

- Century does not manage investments on behalf of clients.

- Century does not solicit funds or guarantee investment returns.

- Century does not accept or make payments in cash, cryptocurrency, or digital assets.

- We do not conduct business via social media or messaging platforms.

Our only official website is www.century.ae, and all communication is conducted exclusively through verified channels.

We strongly urge the public to remain vigilant, verify the authenticity of any communication claiming to be from Century, and report any suspicious activity. Century disclaims any responsibility for losses arising from dealings with unauthorised or fraudulent parties.