Wednesday, March 11, 2026

GBAB Municipal Bond Fund - An Income Idea In Uncertain Times

By Century Financial in 'Investment Insights'

Executive Summary

As the US-Israel military campaign against Iran disrupts global energy flows and fractures the traditional safe-haven playbook, GBAB's domestic municipal bond portfolio stands uniquely insulated from the chaos. The fund offers near-double-digit yield.

The Key Thesis

Municipal bonds are likely to remain stable as their revenues derive from domestic taxes and essential services not global commodity flows. This divergence creates an opportunity for income-focused investors.

Oil Spike Lifts US Yields and Dollar

.png)

Source: Bloomberg

The Geopolitical Catalyst

Coordinated U.S.-Israeli strikes on Iran triggered an immediate supply shock, tanker traffic through the Strait of Hormuz effectively halted, shipping and refinery operations were disrupted, and markets repriced energy and safe haven assets sharply higher; major banks warned that even partial disruptions could materially lift oil’s fair value, while the administration signaled mitigation measures with Strategic Petroleum Reserve releases on standby a near term backstop that may cap extremes but does not eliminate medium term upside risks to inflation, tighter global financial conditions, and pressure on energy importing economies.

Investment Outlook

The convergence of a geopolitical energy shock, and exceptionally strong municipal credit fundamentals positions GBAB as a compelling income vehicle for the current environment. The fund's 9.91% yield, monthly payout cadence, domestic revenue insulation, and Build America Bond scarcity premium create a differentiated value proposition that few fixed-income alternatives can match.

In a war that is breaking the safe-haven trading ideas, municipal bonds represent a domestic safe haven backed by American tax revenues, essential services, and explicit federal subsidies rather than global commodity flows.

Municipal bonds derive their cash flows entirely from U.S. dollar-denominated revenue streams, property taxes, sales taxes, individual and corporate income taxes, and user fees collected within the United States. State total cash balances a combination of rainy-day reserves and general fund ending balances remain near record highs heading into 2026. This means GBAB's underlying credits are backed by a massive, diversified, and purely dollar-based domestic tax collection apparatus that is structurally insulated from foreign-exchange volatility, commodity price swings, and the geopolitical dislocations currently roiling global markets. The dollar-denominated, domestically sourced income underpinning municipal bonds provides an anchor of stability.

For income-focused investors seeking to position defensively while maintaining near-double-digit yield, GBAB represents a timely opportunity at the intersection of geopolitical dislocation and fundamental municipal credit strength.

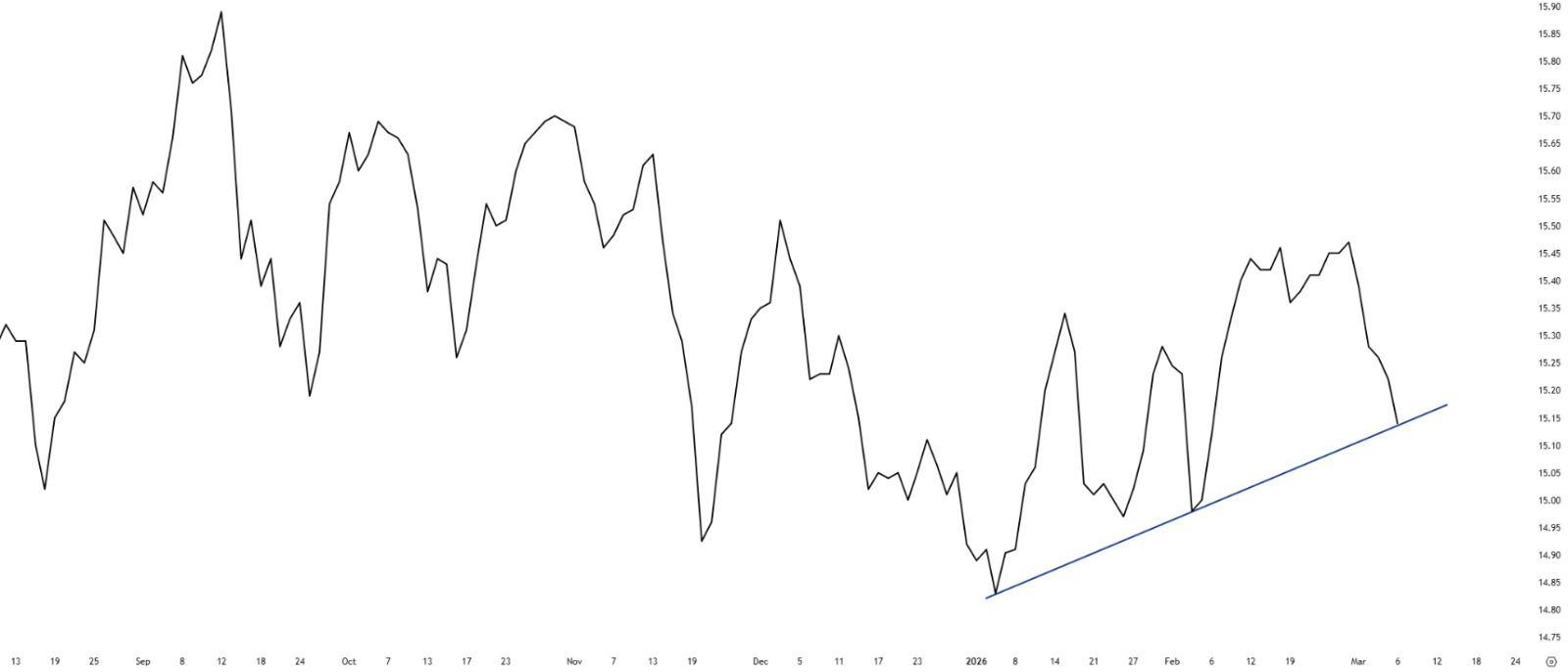

GBAB CHART

The Municipal Bond Advantage: Structural Immunity to the Oil Shock

GBAB’s bullish case rests on its concentrated exposure to taxable municipal credit, notably a large allocation to Build America Bonds, which ties cash flows to domestic tax receipts, user fees, and federally subsidized interest rather than to commodity exporters or foreign sovereigns, materially reducing direct transmission from Middle Eastern oil shocks to issuer revenues.

The fund’s portfolio construction and monthly distribution profile reflect that orientation, GBAB reports a high current distribution rate and a NAV/market price that show investor demand for taxable muni yield in a low supply environment.

Build America Bonds add a structural credit buffer because of the federal interest subsidy paid to issuers and the program’s finite supply factors that support scarcity value, broaden the buyer base beyond tax exempt muni investors, and can enhance liquidity during risk episodes.

Combined with generally strong municipal balance sheets and elevated ratings across the index, GBAB’s emphasis on investment grade, subsidy backed issues positions it to weather Treasury repricings driven by geopolitics better than corporate or sovereign credit with direct energy exposure.

| Time Period | Return (%) |

|---|---|

| 1 Week | -1.49% |

| 1 Month | 2.29% |

| 3 Months | 1.35% |

| YTD | 3.69% |

| 1 Year | 6.47% |

| 3 Year | 6.45% |

| 5 Year | 0.22% |

| Companies | Weight (%) |

|---|---|

| 12 Month Yield | 9.91% |

| Indicated Yield | 9.91% |

| 1 Yr Dividend Growth | 0% |

| 3 Yr Dividend Growth | 0% |

| 5 Yr Dividend Growth | 0% |

| Last Price | USD 15.22 |

| Payment Frequency | Monthly |

| Sector | Weight (%) |

|---|---|

| Municipal | 65.44% |

| Other ABS | 10.94% |

| Insurance | 8.92% |

| Healthcare-Services | 6.11% |

| Diversified Financial Services | 4.77% |

| Electric | 3.08% |

| Companies | Weight (%) |

|---|---|

| West Virginia Higher Education Policy Commission 7.65 04/ | 1.96% |

| Dallas Convention Center Hotel Development Corp 7.09 01/ | 1.90% |

| School District of Philadelphia/The 6 09/01/2030 | 1.85% |

| Oklahoma Development Finance Authority 5.45 08/15/2028 | 1.82% |

| Oakland Unified School District/Alameda County 6.88 08/0 | 1.69% |

| Westchester County Healthcare Corp/NY 8.57 11/01/2040 | 1.61% |

| Santa Ana Unified School District 7.1 08/01/2040 | 1.50% |

| Evansville-Vanderburgh School Building Corp 6.5 01/15/20 | 1.46% |

| Pittsburgh School District 6.85 09/01/2029 | 1.26% |

| CINCON 3.797 12/31/57 | 1.23% |

| Asset Class | Weight (%) |

|---|---|

| Municipal | 65.44% |

| Corporate | 47.07% |

| Mortgage | 15.23% |

| Government | 1.99% |

| Preferred | 1.39% |

| Equity | 0.62% |

| Region | Weight (%) |

|---|---|

| U.S. | 100% |

Risks and Assumptions related to Back-tested trading strategies

Disclaimer:Century Financial Consultancy LLC (CFC) is licensed and regulated by the Capital Market Authority (CMA) of the UAE under license numbers 20200000028 and 301044 to carry out the activities of Financial Products dealer, Trading Broker in international markets, Trading Broker of OTC derivatives and currencies in the spot market, Introduction, Financial Consultations, and Promotion. CFC is incorporated under UAE law, registered with the Dubai Economic Department (No. 768189), with its office at 601, Level 6, Building No. 4, Emaar Square, Downtown Dubai, UAE, PO Box 65777.

Terms and Conditions of Access

By accessing and continuing to use the Publication (which includes this document, flyer, charts, diagrams, illustrations, images, calculations, scenario analysis, and related data or content), you confirm that you have read, understood, and agreed to the terms of this Disclaimer.

CFC reserves the right to amend or update the Publication and this Disclaimer at any time without prior notice. Continued use following any such update constitutes your acceptance of the revised terms. If you do not agree with these terms, please discontinue use of the Publication.

Purpose and Intended Use

This Publication is classified as marketing material and should not be regarded as independent investment research. It is provided for informational, educational, and illustrative purposes only and does not constitute investment advice, a recommendation, an offer, or a solicitation to buy or sell any financial instruments or services. All views expressed are general market commentary and may not reflect the opinions of CFC as a whole.

Risk Disclosures and Limitations

The information presented does not cover all the risks associated with the products or scenarios discussed. Please refer to the full Risk Disclosure Statement available on our website.

This Publication reflects information available at the time of preparation and does not account for subsequent developments. Any forward-looking statements involve assumptions and uncertainties; actual outcomes may differ materially. CFC does not guarantee the accuracy, completeness, or reliability of the information and disclaims liability for any action taken based on it.

No Offer or Contractual Commitment

No part of this Publication constitutes an offer, agreement, or commitment to enter into any transaction. Distribution of this Publication does not oblige CFC to engage in any trade or provide any services. Product names or terms may differ across platforms or providers. This material should not be interpreted as legal, regulatory, tax, accounting, or credit advice. Recipients should seek independent professional advice and assess their own financial situation, objectives, and risk profile before making investment decisions.

Data Sources and Interpretation

This Publication may rely on publicly available data, third-party information, or model-based assumptions. CFC makes no representation or warranty as to their accuracy or completeness. Data limitations, errors, or outdated inputs may impact the reliability of projections or scenarios. Names of financial products may differ from those used on trading platforms.

Use, Reproduction, and Analyst Disclosure

This Publication is intended solely for the recipient’s informational use. It may not be copied, transmitted, or distributed in any form, wholly or partially, without prior written permission from CFC.

Analyst Declaration: The Analyst(s) certifies that all opinions expressed in this Publication represent their own independent views and that reasonable care was taken to ensure objectivity. They do not hold securities in the companies mentioned, and their compensation is not linked to the views expressed. CFC’s research and marketing divisions operate independently.

Trading Risk Warning:

Trading in financial products involves significant risk. Leveraged OTC derivatives, such as Contracts for Difference (CFDs) and spot forex contracts, carry a high risk of loss that can potentially exceed initial deposits and may not be suitable for all investors. These instruments do not confer ownership of underlying assets. Investors must carefully evaluate their investment objectives and risk tolerance, and consult independent advisors where appropriate.

Regulated by CMA

Century Financial Consultancy LLC

.png)

.png)

.png)

.png)

Reach us:

-

Dubai

6th Floor, Emaar Square Building 4,

Downtown, Dubai, P.O. Box 65777,

Dubai, United Arab Emirates -

Abu Dhabi

27th Floor, Office 2701,

Shining Towers, Abu Dhabi, UAE -

Sharjah

29th Floor, Office 2905,

The Business Tower, Sharjah, UAE - +971 (4) 356 2800

- info@century.ae

Disclaimer: Trading in financial products carries substantial risk. Leveraged over-the-counter (OTC) derivatives, such as Contracts for Difference (CFDs) and spot forex, may result in losses exceeding initial deposits and may not be suitable for all investors. These complex instruments do not confer ownership of the underlying assets. Investors should carefully consider their investment objectives and risk appetite, and seek independent professional advice if necessary.

Century Financial Consultancy LLC (CFC) is licensed and regulated by the Capital Market Authority (CMA) of the UAE under license numbers 20200000028 and 301044 to carry out the activities of Financial Products dealer, Trading Broker in international markets, Trading Broker of OTC derivatives and currencies in the spot market, Introduction, Financial Consultations, and Promotion. CFC is incorporated under UAE law, registered with the Dubai Economic Department (No. 768189), with its office at 601, Level 6, Building No. 4, Emaar Square, Downtown Dubai, UAE, PO Box 65777.

The content on this website is provided solely for informational and educational purposes and does not constitute an offer, recommendation, or solicitation to buy or sell any securities or financial products.

Products and services offered by CFC are not intended for use in any jurisdiction where such use or distribution would breach local laws or regulatory requirements.

⚠️ Alert: Fraudulent Activity Notice

Century Financial Consultancy LLC (“Century”) has become aware of fraudulent individuals and entities impersonating our firm through unofficial websites, social media channels, and messaging applications such as Telegram, WhatsApp, and Discord.

Please be advised:

- Century does not manage investments on behalf of clients.

- Century does not solicit funds or guarantee investment returns.

- Century does not accept or make payments in cash, cryptocurrency, or digital assets.

- We do not conduct business via social media or messaging platforms.

Our only official website is www.century.ae, and all communication is conducted exclusively through verified channels.

We strongly urge the public to remain vigilant, verify the authenticity of any communication claiming to be from Century, and report any suspicious activity. Century disclaims any responsibility for losses arising from dealings with unauthorised or fraudulent parties.