Thursday, April 09, 2026

Gold: Preserving Wealth in a Volatile World

By Century Financial in 'Investment Insights'

Introduction

Geopolitical tensions rose dramatically on 28 February 2026 when the United States and Israel carried out coordinated military strikes on Iran under Operation Lion’s Roar. The strikes targeted several key military and strategic facilities. Iran responded quickly with missile and drone attacks across the Gulf region, including strikes on U.S. bases and infrastructure in several countries. The situation also created volatility in energy markets. One major concern is the Strait of Hormuz, a narrow but extremely important shipping route through which around 20% of the world’s oil supply passes. Any disruption there could lead to supply shortages and higher oil prices.

Events like this usually affect financial markets in two phases:

Phase 1 – Liquidity Shock

Right after a geopolitical shock, markets usually react with a broad sell-off. Investors often rush to reduce risk and raise cash. When equity markets fall, leveraged funds may face margin calls and are forced to sell their most liquid assets and recently profitable assets to meet them. This can include gold, which means even safe-haven assets may come under short-term pressure.

At the same time, conflicts can push oil prices higher. Rising oil prices can lift bond yields and strengthen the U.S. dollar. A stronger dollar and higher yields can temporarily limit gold’s upside. We can assume this is the reason gold hasn't rallied yet since the start of the war. Despite the gains in Dollar and yields, gold is holding strong, straying true to its definition of a safe-haven. In this early stage, markets are mostly reacting to short-term liquidity pressures rather than the long-term safe-haven appeal of gold.

Phase 2 – Safe Haven Repricing

Once the initial liquidity shock passes, markets usually move into a second phase. At this stage, investors begin to fully price in the geopolitical risks. Money slowly starts shifting toward defensive assets such as gold

History shows that gold often performs well during long periods of conflict and uncertainty.

| Conflict / Event | War / Event Start | Gold Price at Start | Rally High | Peak Date | Approx. Gain |

|---|---|---|---|---|---|

| Iranian Revolution & Oil Crisis | Jan-79 | ~$226/oz | ~$850/oz | Jan-80 | ~+275% |

| Afghanistan War (US invasion) | Oct-01 | ~$270/oz | ~$417/oz | Dec-03 | ~+50% |

| Iraq War | Mar-03 | ~$340/oz | ~$730/oz | May-06 | ~+115% |

| Global Financial Crisis | Aug-07 | ~$700/oz | ~$1,920/oz | Sep-11 | ~+174% |

| Russia–Ukraine War | Feb-22 | ~$1,800/oz | ~$5,600/oz | Jan-26 | ~+211% |

One reason gold attracts demand during these periods is because it is not tied to the credit risk of any government or financial institution. This makes it a trusted store of value when confidence in currencies or financial systems weakens.

Wars often lead to higher oil prices, rising inflation, and increased government spending. These factors can weaken currencies and encourage institutional investors and central banks to increase their gold holdings. Because of this, gold has consistently acted as a global hedge against geopolitical risk, inflation, and currency volatility.

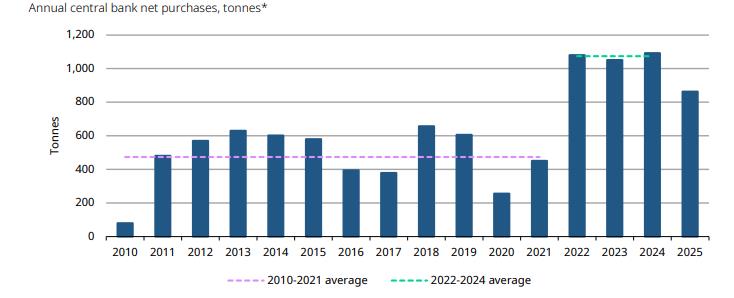

Central Banks Accelerate Gold Buying as Geopolitical Uncertainty Rises

Source: World Gold Council

The chart shows a sharp rise in central bank gold purchases over the past few years. After averaging roughly 450 tonnes annually between 2010 and 2021, purchases surged to over 1,000 tonnes from 2022 - 25. This reflects rising safe-haven demand amid geopolitical uncertainty and wars, a trend that may continue into 2026 as global risks remain elevated.

Gold vs Fiat Currencies: A Long-Term Store of Purchasing Power

.png)

Source: LBMA, U.S. Bureau of Labor Statistics, RBI.

Since the end of the gold standard in 1971, gold has maintained its purchasing power better than fiat currencies, notably the dollar. Gold prices have risen from about $35 per ounce in 1971 to nearly $5,200 today, reflecting its long-term role as a store of value. As can be observed in the above chart, in the same period, the dollar lost approximately 83% of its value/purchasing power due to inflation while many of the currencies of emerging markets lost even more than that. The rupee has been one of them and has become significantly weaker against both the dollar and gold, over time.

The recent increase in geopolitical tension has also exposed the rupee's vulnerability. Within the span of two weeks, the rupee depreciated from around ₹90 per USD to almost ₹93 per USD. For expats, looking to safeguard against rupee depreciation, gold can be a great option.

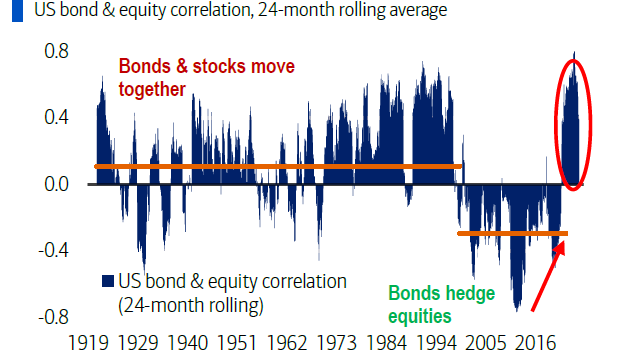

Gold Replacing Bonds as the Market Hedge

Source: LBMA, U.S. Bureau of Labor Statistics, RBI.

Recently, gold has also increasingly replaced bonds as a hedge against equities. The traditional negative correlation between bonds and stocks has weakened, and both asset classes now often move in the same direction. In this environment, gold is gaining importance as a portfolio hedge, offering protection against equity volatility, inflation, and geopolitical risks.

Outlook:

Gold has long been seen as a reliable store of value, especially during times of geopolitical tension and economic uncertainty. When conflicts last longer, inflation risks rise and currencies become unstable, investors often turn to gold for safety. In recent years, central banks have also been increasing their gold purchases, which has added further support to demand. Because of these factors, gold continues to play an important role as a strategic asset in uncertain and volatile global markets. Gold’s ability to hold its purchasing power over long periods is another reason why it remains attractive.

Risks and Assumptions related to Back-tested trading strategies

Disclaimer:Century Financial Consultancy LLC (CFC) is licensed and regulated by the Capital Market Authority (CMA) of the UAE under license numbers 20200000028 and 301044 to carry out the activities of Financial Products dealer, Trading Broker in international markets, Trading Broker of OTC derivatives and currencies in the spot market, Introduction, Financial Consultations, and Promotion. CFC is incorporated under UAE law, registered with the Dubai Economic Department (No. 768189), with its office at 601, Level 6, Building No. 4, Emaar Square, Downtown Dubai, UAE, PO Box 65777.

Terms and Conditions of Access

By accessing and continuing to use the Publication (which includes this document, flyer, charts,

diagrams, illustrations, images, calculations, scenario analysis, and related data or content), you

confirm that you have read, understood, and agreed to the terms of this Disclaimer.

CFC reserves the right to amend or update the Publication and this Disclaimer at any time without

prior notice. Continued use following any such update constitutes your acceptance of the revised

terms. If you do not agree with these terms, please discontinue use of the Publication.

Purpose and Intended Use

This Publication is classified as marketing material and should not be regarded as independent

investment research. It is provided for informational, educational, and illustrative purposes only

and does not constitute investment advice, a recommendation, an offer, or a solicitation to buy or

sell any financial instruments or services. All views expressed are general market commentary and

may not reflect the opinions of CFC as a whole.

Risk Disclosures and Limitations

The information presented does not cover all the risks associated with the products or scenarios

discussed. Please refer to the full Risk

Disclosure Statement available on our website.

This Publication reflects information available at the time of preparation and does not account for

subsequent developments. Any forward-looking statements involve assumptions and uncertainties;

actual outcomes may differ materially. CFC does not guarantee the accuracy, completeness, or

reliability of the information and disclaims liability for any action taken based on it.

No Offer or Contractual Commitment

No part of this Publication constitutes an offer, agreement, or commitment to enter into any

transaction. Distribution of this Publication does not oblige CFC to engage in any trade or provide

any services. Product names or terms may differ across platforms or providers. This material should

not be interpreted as legal, regulatory, tax, accounting, or credit advice. Recipients should seek

independent professional advice and assess their own financial situation, objectives, and risk

profile before making investment decisions.

Data Sources and Interpretation

This Publication may rely on publicly available data, third-party information, or model-based

assumptions. CFC makes no representation or warranty as to their accuracy or completeness. Data

limitations, errors, or outdated inputs may impact the reliability of projections or scenarios.

Names of financial products may differ from those used on trading platforms.

Use, Reproduction, and Analyst Disclosure

This Publication is intended solely for the recipient’s informational use. It may not be copied,

transmitted, or distributed in any form, wholly or partially, without prior written permission from

CFC.

Analyst Declaration: The Analyst(s) certifies that all opinions expressed in this Publication represent their own independent views and that reasonable care was taken to ensure objectivity. They do not hold securities in the companies mentioned, and their compensation is not linked to the views expressed. CFC’s research and marketing divisions operate independently.

Trading Risk Warning:

Trading in financial products involves significant risk. Leveraged OTC derivatives, such as

Contracts for Difference (CFDs) and spot forex contracts, carry a high risk of loss that can

potentially exceed initial deposits and may not be suitable for all investors. These instruments do

not confer ownership of underlying assets. Investors must carefully evaluate their investment

objectives and risk tolerance, and consult independent advisors where appropriate.

Regulated by CMA

Century Financial Consultancy LLC

.png)

.png)

.png)

.png)

.png)

Reach us:

-

Dubai

6th Floor, Emaar Square Building 4,

Downtown, Dubai, P.O. Box 65777,

Dubai, United Arab Emirates -

Abu Dhabi

27th Floor, Office 2701,

Shining Towers, Abu Dhabi, UAE -

Sharjah

29th Floor, Office 2905,

The Business Tower, Sharjah, UAE - +971 (4) 356 2800

- info@century.ae

Disclaimer: Trading in financial products carries substantial risk. Leveraged over-the-counter (OTC) derivatives, such as Contracts for Difference (CFDs) and spot forex, may result in losses exceeding initial deposits and may not be suitable for all investors. These complex instruments do not confer ownership of the underlying assets. Investors should carefully consider their investment objectives and risk appetite, and seek independent professional advice if necessary.

Century Financial Consultancy LLC (CFC) is licensed and regulated by the Capital Market Authority (CMA) of the UAE under license numbers 20200000028 and 301044 to carry out the activities of Financial Products dealer, Trading Broker in international markets, Trading Broker of OTC derivatives and currencies in the spot market, Introduction, Financial Consultations, and Promotion. CFC is incorporated under UAE law, registered with the Dubai Economic Department (No. 768189), with its office at 601, Level 6, Building No. 4, Emaar Square, Downtown Dubai, UAE, PO Box 65777.

The content on this website is provided solely for informational and educational purposes and does not constitute an offer, recommendation, or solicitation to buy or sell any securities or financial products.

Products and services offered by CFC are not intended for use in any jurisdiction where such use or distribution would breach local laws or regulatory requirements.

⚠️ Alert: Fraudulent Activity Notice

Century Financial Consultancy LLC (“Century”) has become aware of fraudulent individuals and entities impersonating our firm through unofficial websites, social media channels, and messaging applications such as Telegram, WhatsApp, and Discord.

Please be advised:

- Century does not manage investments on behalf of clients.

- Century does not solicit funds or guarantee investment returns.

- Century does not accept or make payments in cash, cryptocurrency, or digital assets.

- We do not conduct business via social media or messaging platforms.

Our only official website is www.century.ae, and all communication is conducted exclusively through verified channels.

We strongly urge the public to remain vigilant, verify the authenticity of any communication claiming to be from Century, and report any suspicious activity. Century disclaims any responsibility for losses arising from dealings with unauthorised or fraudulent parties.