Wednesday, April 29, 2026

Hormuz Crisis: Oil at the Tipping Point

By Century Financial in 'Investment Insights'

Current Scenario

Global oil markets remain under acute pressure as geopolitical risks compound an already severe supply shock triggered by the U.S.–Iran war, which began on Feb. 28. Hopes for near-term stabilization briefly improved following a tentative ceasefire announced on April 7, but those expectations have since faded. The U.S. has kept a naval blockade on Iranian ports in place, sustaining disruption across key Middle Eastern export routes and keeping tanker traffic through the Strait of Hormuz well below pre-war levels.

The market is now absorbing what is effectively the largest supply disruption on record, with global oil supply estimated to be 10.8 million barrels a day below baseline. The blockade is widely viewed as leverage to bring Tehran back to the negotiating table. A second round of talks is expected in the coming days; uncertainty and escalation risks remain high.

Markets appear to be pricing in a premature resolution rather than a real recovery in physical flows, leaving a clear gap between paper and spot prices. While a ~400 million-barrel SPR release initially cushioned the shock, it has been offset by ~550 million barrels (11 mb/d over ~50 days) of cumulative supply losses. The balance ~150 million barrels has been showing up in the form of onshore inventory drawdowns.

With Gulf production unlikely to return before end-June, supply remains structurally constrained. As buffers are depleted and spare capacity is minimal, oil prices are likely to stay elevated, with further upside risk as tight physical conditions persist.

Shrinking Inventories Drive Oil Higher

Oil prices are currently being driven by scenario-based expectations around the recovery of flows through the Strait of Hormuz. Oil is expected to trade within a wide $70 to $150+ range, depending on the extent and duration of disruption.

The following scenarios assess probable Crude oil price ranges over the next 1–3 months, contingent on the trajectory of Strait of Hormuz shipping flows following a ceasefire agreement. Each scenario reflects a distinct supply-side outcome and associated market risk premium.

| Scenario | Hormuz Flows |

Market Impact | Brent Oil Range (1–3 months) |

|---|---|---|---|

| Full Normalization(low probability) |

Near full recovery |

Supply returns and logistical constraints ease. Shipping and loading frictions subside, stabilising market conditions.Risk premium declines; backwardation softens. | $80 – $90per barrel |

| Partial Recovery | Uneven / constrained |

Backlogs clear but shipping and loading frictions persist. Supply improves without fully normalizing, sustaining elevated prices.Continued volatility; firm backwardation expected. | $90 – $110per barrel |

| Renewed Disruption |

Flows stall / fall | Supply tightens again as flows stall or decline further, pushing risk premiums sharply higher. Extended disruption could drive prices toward $150+.Risk premium surges; supply crunch scenario. | $110+per barrel |

Key Observations

- Full normalisation represents the base case for supply recovery and risk premium compression, anchoring Brent in the $80–$90 range.

- Partial recovery is the most likely near-term path, with persistent frictions keeping backwardation firm and prices elevated in the $90–$110 corridor.

- Renewed disruption carries meaningful tail risk, with prices breaching $110 and potentially approaching $150+ under an extended supply shock.

Escalation as a Direct Upside Trigger

In the event of further geopolitical escalation, oil prices are likely to move sharply higher as the market transitions from an already tight balance into an acute supply shock. With an existing deficit of approximately 11–13 mb/d, including 1.6–2 mb/d Iranian oil, the system is operating with minimal flexibility, leaving it highly vulnerable to any incremental disruption.

Further escalation, through Hormuz disruptions, tighter Iranian export constraints, or broader regional spillovers, would materially widen the supply deficit and exacerbate market imbalance.

The ongoing US naval blockade itself introduces an additional layer of structural risk. While the blockade is intended to pressure Iran into concessions, compliance remains unlikely, as doing so would imply significant economic losses, estimated at roughly $150–160 million per day in lost oil export revenues, based on ~1.6 mb/d of exports priced at ~$95–100 per barrel. Although Iran retains some flexibility through alternative non-oil exports and limited crude already at sea, the risk of expanded US enforcement, including potential global interception of Iranian vessels, raises the probability of a prolonged and more severe supply disruption.

At the same time, with spare capacity nearly exhausted and global inventories already drawing down, the oil market lacks the buffers required to absorb further shocks. This implies that any incremental disruption would translate almost directly into price.

As a result, escalation acts as a clear and immediate catalyst for higher oil prices, triggering:

- Sharper backwardation in futures markets

- Further widening of physical premiums

- Accelerated repricing across benchmarks

In this context, oil becomes highly sensitive to marginal changes in supply, and escalation could drive a nonlinear price spike, potentially pushing the market more rapidly toward demand-destruction levels.

Post-De-Escalation Dynamics: A Market Still in Deficit

Even in the event of geopolitical de-escalation, oil markets are likely to remain structurally tight with significant upside risk, as the underlying supply-demand imbalance persists.

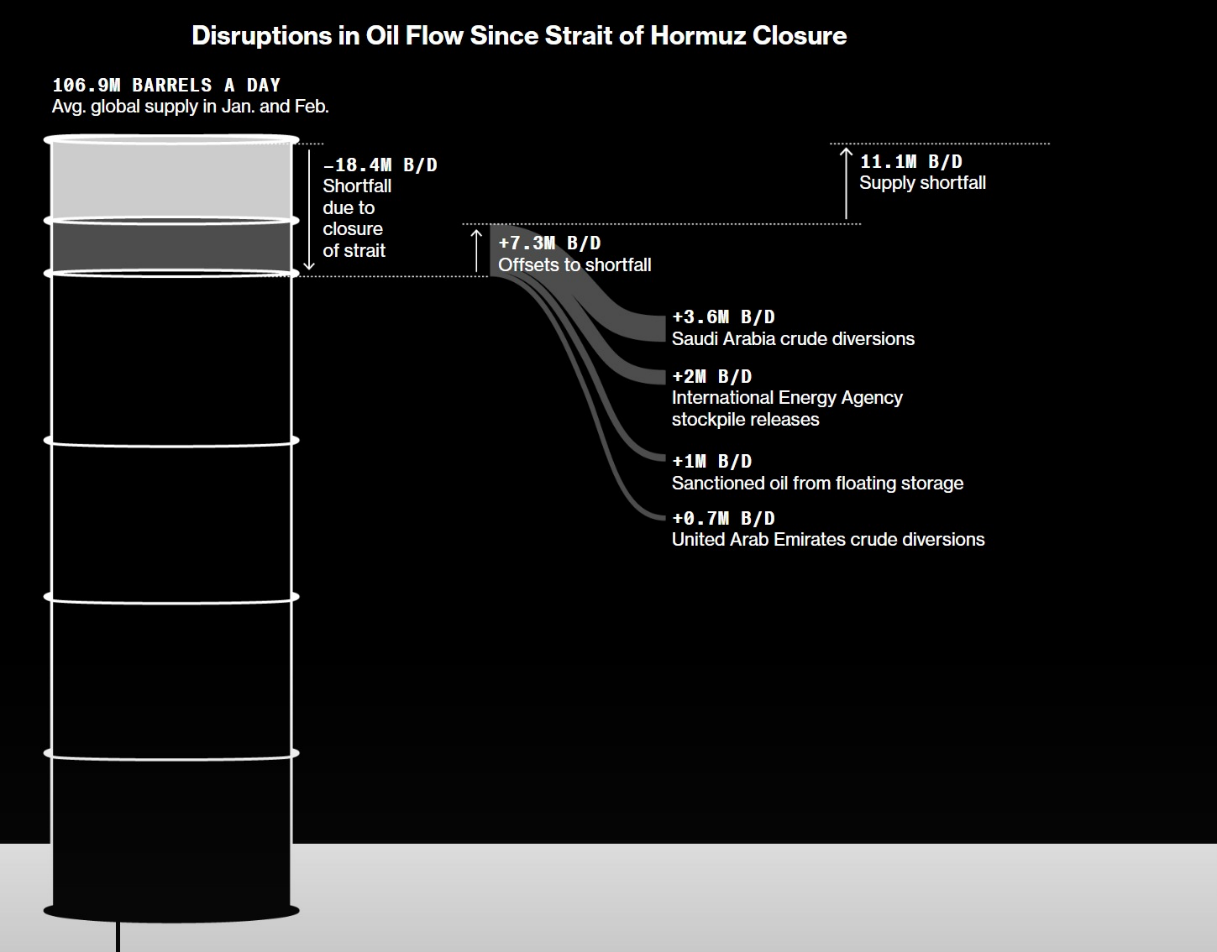

The closure of the Strait of Hormuz initially removed approximately 18.4 mb/d of crude flows, of which only 7.3 mb/d has been offset through emergency measures, leaving a net shortfall of 11.1 mb/d. Additionally, after accounting for Iranian output that is stuck due to the US naval blockade, there is a 13 mb/d structural supply shock.

Even with a ceasefire, shut-in production cannot return immediately, with restart timelines extending to end-June or beyond, keeping the market undersupplied.

At the same time, global buffers have largely been exhausted, with a 400 million-barrel global SPR release only delaying the adjustment by 2–3 weeks, and both floating storage and onshore inventories now entering sustained drawdowns. Crucially, the disruption has not only reduced supply but also fragmented global flows, creating a shortage of deliverable crude outside the Gulf, even as stranded barrels remain inaccessible within the region.

This has already begun to manifest in tightening refining margins and product markets, particularly in Asia, where a refined product crisis is expected within weeks.

Importantly, financial markets continue to lag these physical dynamics, with crude benchmarks still pricing in partial normalisation despite a $30+/bbl premium in physical markets and confirmed export losses of ~9 mb/d.

As inventory draws become more visible, particularly as US commercial crude stocks approach the 400-million-barrel Cushing operational floor, the market is likely to reprice rapidly. As of 10 April 2026, US commercial crude inventories were reported at 463.8 million barrels by the EIA. Provided that the Strait of Hormuz flows do not return to normal, and physical inventory drawdowns continue, US commercial crude storage will be below ~400 million barrels and approaching the operational minimum of 370 to 380 million barrels by the end of July. This includes an estimated SPR release total of 139 million barrels.

The cumulative storage lost due to the closure is already ~1 billion barrels. This increases to 1.2 billion barrels by the end of April, 1.59 billion barrels by the end of May, and 1.98 billion barrels by the end of June.

There is not enough commercially available crude for that much supply loss. In this context, even with easing geopolitical tensions, the persistence of a large supply deficit, depleted buffers, and delayed supply recovery creates conditions for oil prices to remain elevated and potentially break higher as the market transitions from perceived surplus to confirmed scarcity.

Forward Outlook – Key Takeaways

- Imbalance worsens into end-April: Ongoing disruptions → accelerating inventory drawdowns

- Critical trigger approaching: US crude stocks falling from ~463.8 mb → ~400 mb Cushing floor → rapid market repricing

- Severe supply erosion: ~1 bn barrels already lost, rising toward ~2 bn by June → insufficient commercial supply

- Asia tightening sharply: By early May, only Japan & China hold excess stocks → rest of Asia forced to scramble

- Refinery behaviour shifts: Potential for price-insensitive buying to avoid shutdowns

- SPR = delay, not solution: Additional releases may smooth timing, but do not fix the deficit

- Bottom line: Oil remains structurally tight with strong upside risk, as markets shift from perceived surplus → confirmed scarcity

Risks and Assumptions related to Back-tested trading strategies

Disclaimer: Century Financial Consultancy LLC (CFC) is licensed and regulated by the Capital Market Authority (CMA) of the UAE under license numbers 20200000028 and 301044 to carry out the activities of Financial Products dealer, Trading Broker in international markets, Trading Broker of OTC derivatives and currencies in the spot market, Introduction, Financial Consultations, and Promotion. CFC is incorporated under UAE law, registered with the Dubai Economic Department (No. 768189), with its office at 601, Level 6, Building No. 4, Emaar Square, Downtown Dubai, UAE, PO Box 65777.

Terms and Conditions of Access

By accessing and continuing to use the Publication (which includes this document, flyer, charts, diagrams,

illustrations, images, calculations, scenario analysis, and related data or content), you confirm that you

have read, understood, and agreed to the terms of this Disclaimer.

CFC reserves the right to amend or update the Publication and this Disclaimer at any time without prior

notice. Continued use following any such update constitutes your acceptance of the revised terms. If you do

not agree with these terms, please discontinue use of the Publication.

Purpose and Intended Use

This Publication is classified as marketing material and should not be regarded as independent investment

research. It is provided for informational, educational, and illustrative purposes only and does not

constitute investment advice, a recommendation, an offer, or a solicitation to buy or sell any financial

instruments or services. All views expressed are general market commentary and may not reflect the opinions

of CFC as a whole.

Risk Disclosures and Limitations

The information presented does not cover all the risks associated with the products or scenarios discussed.

Please refer to the full Risk

Disclosure Statement available on our website.

This Publication reflects information available at the time of preparation and does not account for

subsequent developments. Any forward-looking statements involve assumptions and uncertainties; actual

outcomes may differ materially. CFC does not guarantee the accuracy, completeness, or reliability of the

information and disclaims liability for any action taken based on it.

No Offer or Contractual Commitment

No part of this Publication constitutes an offer, agreement, or commitment to enter into any transaction.

Distribution of this Publication does not oblige CFC to engage in any trade or provide any services. Product

names or terms may differ across platforms or providers. This material should not be interpreted as legal,

regulatory, tax, accounting, or credit advice. Recipients should seek independent professional advice and

assess their own financial situation, objectives, and risk profile before making investment decisions.

Data Sources and Interpretation

This Publication may rely on publicly available data, third-party information, or model-based assumptions.

CFC makes no representation or warranty as to their accuracy or completeness. Data limitations, errors, or

outdated inputs may impact the reliability of projections or scenarios. Names of financial products may

differ from those used on trading platforms.

Use, Reproduction, and Analyst Disclosure

This Publication is intended solely for the recipient’s informational use. It may not be copied,

transmitted, or distributed in any form, wholly or partially, without prior written permission from CFC.

Analyst Declaration: The Analyst(s) certifies that all opinions expressed in this Publication represent their own independent views and that reasonable care was taken to ensure objectivity. They do not hold securities in the companies mentioned, and their compensation is not linked to the views expressed. CFC’s research and marketing divisions operate independently.

Trading Risk Warning:

Trading in financial products involves significant risk. Leveraged OTC derivatives, such as Contracts for

Difference (CFDs) and spot forex contracts, carry a high risk of loss that can potentially exceed initial

deposits and may not be suitable for all investors. These instruments do not confer ownership of underlying

assets. Investors must carefully evaluate their investment objectives and risk tolerance, and consult

independent advisors where appropriate.

Regulated by CMA

Century Financial Consultancy LLC

.png)

.png)

.png)

Reach us:

-

Dubai

6th Floor, Emaar Square Building 4,

Downtown, Dubai, P.O. Box 65777,

Dubai, United Arab Emirates -

Abu Dhabi

27th Floor, Office 2701,

Shining Towers, Abu Dhabi, UAE -

Sharjah

29th Floor, Office 2905,

The Business Tower, Sharjah, UAE - +971 (4) 356 2800

- info@century.ae

Disclaimer: Trading in financial products carries substantial risk. Leveraged over-the-counter (OTC) derivatives, such as Contracts for Difference (CFDs) and spot forex, may result in losses exceeding initial deposits and may not be suitable for all investors. These complex instruments do not confer ownership of the underlying assets. Investors should carefully consider their investment objectives and risk appetite, and seek independent professional advice if necessary.

Century Financial Consultancy LLC (CFC) is licensed and regulated by the Capital Market Authority (CMA) of the UAE under license numbers 20200000028 and 301044 to carry out the activities of Financial Products dealer, Trading Broker in international markets, Trading Broker of OTC derivatives and currencies in the spot market, Introduction, Financial Consultations, and Promotion. CFC is incorporated under UAE law, registered with the Dubai Economic Department (No. 768189), with its office at 601, Level 6, Building No. 4, Emaar Square, Downtown Dubai, UAE, PO Box 65777.

The content on this website is provided solely for informational and educational purposes and does not constitute an offer, recommendation, or solicitation to buy or sell any securities or financial products.

Products and services offered by CFC are not intended for use in any jurisdiction where such use or distribution would breach local laws or regulatory requirements.

⚠️ Alert: Fraudulent Activity Notice

Century Financial Consultancy LLC (“Century”) has become aware of fraudulent individuals and entities impersonating our firm through unofficial websites, social media channels, and messaging applications such as Telegram, WhatsApp, and Discord.

Please be advised:

- Century does not manage investments on behalf of clients.

- Century does not solicit funds or guarantee investment returns.

- Century does not accept or make payments in cash, cryptocurrency, or digital assets.

- We do not conduct business via social media or messaging platforms.

Our only official website is www.century.ae, and all communication is conducted exclusively through verified channels.

We strongly urge the public to remain vigilant, verify the authenticity of any communication claiming to be from Century, and report any suspicious activity. Century disclaims any responsibility for losses arising from dealings with unauthorised or fraudulent parties.