Wednesday, April 08, 2020

Netflix vs Disney’s Share Price: Which Stock is a Better Quarantine Buy?

By Century Financial in 'Brainy Bull'

Streaming platforms are experiencing a boost as millions around the world are forced to stay indoors. Netflix’s [NFLX] share price has made gains in 2020 while Disney’s [DIS] share price has fallen, however, the winner is far from obvious.

A quick glance at the share price performances of Disney and Netflix in 2020, and it seems there is an obvious frontrunner. Netflix gained 13.5% from the start of the year to 2 April, while the Disney, along with hundreds of other top companies dragged down by the Coronavirus pandemic, has fallen by 33%.

However, as tempting as it can be to pit these two streaming rivals against each other on such simple terms, the bigger picture is much more complex.

Disney, unlike Netflix, is not just a streaming and production company, but an all-round experiential entertainment business that includes theme parks and multiplex experiences. While Disney’s streaming service Disney+ is thriving, the other segments of its business have been hit badly by the pandemic, leading its share price to flounder.

Netflix is king

The platform is not just outpacing Disney so far in 2020, but the entire FAANG collective. While it grew 13.5% up to 2 April, Facebook [FB] dropped by 23.5%, Apple [AAPL] by 17.3%, Google parent Alphabet [GOOG] by 16.5%, and Amazon [AMZN] — the only other riser — rose by just over 2%. This makes a stark difference to 2019, where Netflix posted lower growth than the overall S&P 500 for the year.

In fact, the company is now one of the few businesses that’s expected to stick to its guidance figures for the year after the coronavirus ravaged corporates around the world. Financial research firm Trefis expects that Netflix will not only deliver its guidance numbers, but it says the streamer — which has roughly 167 million users — is likely to surpass expectations when it comes to adding new subscribers this year.

It’s hard to see the downside for Netflix at the moment.

The key disruption is likely to come in the form of a slowdown in production activity — an area the company is aware of, having offered $100m to support cast and crew that have suddenly found themselves out of work as production schedules are cancelled. But even here, the company has stated that it has a pipeline of new content in place that is yet to be released that could stretch for months. The platform also has a wealth of still-popular shows in its library.

Some have gone as far as to predict that Netflix will see increased cash flow during the next few months. The streamer is likely to see not only more sign-ups than usual to the service, but also fewer cancellations, which may result in higher revenues overall, Andrew Tseng writes in the Motley Fool. With all production ceased due to the coronavirus pandemic and lockdown rules, it also means the company is investing less in original content for a few months, reducing its outflows.

The stock is currently approaching its multi-year range resistance, around the $380 to $385 zone, according to The Street. It’s a level the stock has not surpassed for several years, according to Bret Kenwell, apart from a brief period in 2018. If the shares can break out beyond this mark, Netflix has the potential to surge above as high as $400, he says.

Netflix’s underwhelming 2019 performance was largely to do with rising competition. While coronavirus has boosted the stock, the streamer has yet to face the launches of competing platforms Quibi, Peacock and HBO Max, which are likely to have an impact on it in the near future.

Disney is down, but not out

Disney’s streaming service Disney+ has had a spectacular few months since its US launch in November, amassing nearly 30 million subscribers in just three months.

The platform’s March launch in Europe (across the UK, Ireland, Germany, Italy, Spain, Austria and Switzerland) coincided with lockdown measures implemented by governments. Research from Nokia Deepfield recently showed that Disney+ currently accounts for 18% of all internet video traffic in some of these countries.

The platform’s focus on family-friendly content is likely serving it well, with so many children currently home from school. With its India launch coming soon as well, Disney+ could catch up to Netflix in terms of subscriber numbers pretty quickly.

If its streaming segment were the only consideration, there’s no doubt its share price performance would be higher today.

Sadly, other segments of Disney’s business have been hit hard by the pandemic. Some of its theme parks have been shut since January, its multiplex projectors have been closed down and its sports programming is struggling as major events are being cancelled.

With a recession on the horizon, fewer people are likely to participate in these experiences even after the dust of the pandemic has settled. Rick Munarriz, writing in the Motley Fool, believes it could take up to two years for Disney to get back on its feet.

The bright side? Disney is a responsible company acting fast to reduce damage to its business. The company raised a $6bn debt offering and its key executives have taken a pay cut — chairman Bob Iger has forgone his salary entirely. In addition, Disney is a valuable company with enduring brands, making it a good long-term play, especially at a discounted price.

A number crunch

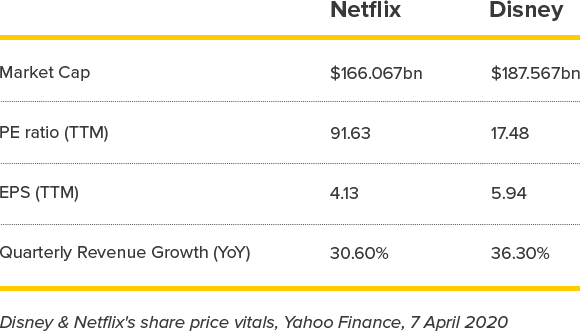

Disney is currently selling at a low price with a price-to-earnings (P/E) ratio of 15.83, compared to Netflix’s 87.90. Netflix temporarily surpassed Disney’s market cap on 30 March. However, for the time being, Disney is back on top with a $169.7bn valuation compared to Netflix’s $159.3bn.

By the end of last year, Netflix reported $16.37bn in debt. This was dwarfed by Disney, which currently carries $51.93bn debt. However, a large part of this is a result of Disney’s recent acquisition of 20th Century Fox.

Morgan Stanley analyst Benjamin Swinburne reduced Disney’s share price target from $170 to $130 on 1 April but reaffirmed his overweight rating for the stock. On the same day, Bernstein analyst Todd Juenger upped his price target on Netflix from $423 to $487.

Source: This content has been produced by Opto trading intelligence for Century Financial and was originally published on cmcmarkets.com/en-gb/opto

Disclaimer: Past performance is not a reliable indicator of future results.

The material (whether or not it states any opinions) is for general information purposes only and does not take into account your personal circumstances or objectives. Nothing in this material is (or should be considered to be) financial, investment or other advice on which reliance should be placed. No opinion given in the material constitutes a recommendation by Century Financial or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person.

Century Financial does not endorse or offer opinion on the trading strategies used by the author. Their trading strategies do not guarantee any return and Century Financial shall not be held responsible for any loss that you may incur, either directly or indirectly, arising from any investment based on any information contained herein.

Regulated by SCA

Century Financial Consultancy LLC

Reach us:

-

Dubai

6th Floor, Emaar Square Building 4,

Downtown, Dubai, P.O. Box 65777,

Dubai, United Arab Emirates -

Abu Dhabi

27th Floor, Office 2701,

Shining Towers, Abu Dhabi, UAE - +971 (4) 356 2800

- info@century.ae

Disclaimer: Trading in financial products carries substantial risk. Leveraged over-the-counter (OTC) derivatives, such as Contracts for Difference (CFDs) and spot forex, may result in losses exceeding initial deposits and may not be suitable for all investors. These complex instruments do not confer ownership of the underlying assets. Investors should carefully consider their investment objectives and risk appetite, and seek independent professional advice if necessary.

Century Financial Consultancy LLC (CFC) is licensed and regulated by the Securities and Commodities Authority (SCA) of the UAE under license numbers 20200000028 and 301044 to carry out the activities of Trading Broker in international markets, Trading Broker of OTC derivatives and currencies in the spot market, Introduction, Financial Consultations, and Promotion. CFC is incorporated under UAE law, registered with the Dubai Economic Department (No. 768189), with its office at 601, Level 6, Building No. 4, Emaar Square, Downtown Dubai, UAE, PO Box 65777.

The content on this website is provided solely for informational and educational purposes and does not constitute an offer, recommendation, or solicitation to buy or sell any securities or financial products.

Products and services offered by CFC are not intended for use in any jurisdiction where such use or distribution would breach local laws or regulatory requirements.

Alert: Fraudulent Activity Notice

Century Financial Consultancy LLC (“Century”) has become aware of fraudulent individuals and entities impersonating our firm through unofficial websites, social media channels, and messaging applications such as Telegram, WhatsApp, and Discord.

Please be advised:

- Century does not manage investments on behalf of clients.

- Century does not solicit funds or guarantee investment returns.

- Century does not accept or make payments in cash, cryptocurrency, or digital assets.

- We do not conduct business via social media or messaging platforms.

Our only official website is www.century.ae, and all communication is conducted exclusively through verified channels.

We strongly urge the public to remain vigilant, verify the authenticity of any communication claiming to be from Century, and report any suspicious activity. Century disclaims any responsibility for losses arising from dealings with unauthorised or fraudulent parties.