Wednesday, July 22, 2020

Will Microsoft’s share price spike again on robust cloud earnings?

By Century Financial in 'Brainy Bull'

Microsoft’s [MSFT] share price has climbed 31.74% YTD to close at $211.60 on 20 July, outstripping the performance of the Nasdaq which only rose 21.78% in the same period.

While the COVID-19 pandemic was in full swing and people were sheltering at home, Microsoft’s share price benefited from an increased use of cloud services and remote working tools.

Since March’s pandemic market sell-off, Microsoft’s share price rose 29% in the three months to the end of June. Momentum has slowed down in July, however, with Microsoft’s share price up by just 3.4% so far this month (through 20 July’s close).

Will the company’s Q4 fiscal 2020 earnings report, due on 22 July, help Microsoft’s share price regain momentum?

Minimal impact from COVID-19 in Q3

For its Q3 2020 earnings report, Microsoft posted total revenue of $35bn, which marked a 15% year-over-year increase. It also surpassed the $33.66bn expected by analysts polled by Refinitiv, according to CNBC.

Personal computing revenue was $11bn — a 3% year-over-year increase — and productivity and business processes accounted for $11.7bn — a 15% increase on the same period a year ago.

The company’s intelligent cloud was the best performing segment, rising 27% year-over-year to $12.3bn. One of its biggest products in the intelligent cloud segment is Azure, which saw its revenue for the quarter rise by 59% from the same period a year ago.

Growth in these segments was key to Microsoft’s share price success in Q3, although the company had yet to see any real impact from COVID-19 in this quarter.

For Q4, the company expects intelligent cloud revenue to be between $12.9bn and $13.15bn, while revenue for productivity and business processes is set to reach between $11.65bn and $11.95bn, figures which suggest Microsoft’s share price could be set for a boost.

As of 20 July, the average analyst estimate for Q4 revenue is $36.5bn, with the average earnings estimate, pegged at $1.38 a share, according to data from Yahoo Finance.

Indications are that the company is on track to meet its guidance, spurred on by the number of people transitioning to working from home and relying on virtual meetings. If the tech giant does achieve these figures, a drop in Microsoft’s share price would be surprising.

During the Q3 earnings call, Satya Nadella, CEO of Microsoft, noted that on its video-messaging platform Teams 4.1 billion meeting minutes had been generated by 200 million meeting participants in a single day in April. “Teams now has more than 75 million daily active users,” Nadella said.

Missing earnings predictions may not be detrimental to growth

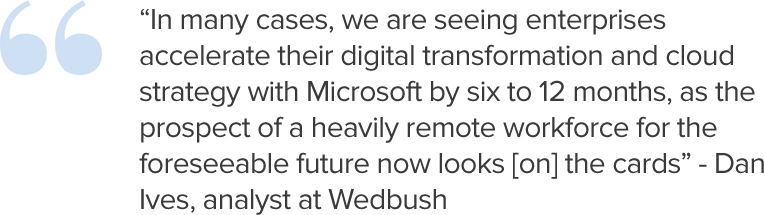

High user growth, coupled with an increase in the number of subscriptions being taken out for other products, such as Azure, signifies “relatively strong cloud deal activity,” wrote Dan Ives, analyst at Wedbush, in a note to clients. He recently reiterated an outperform rating and raised his price target from $240 to $260.

“In many cases, we are seeing enterprises accelerate their digital transformation and cloud strategy with Microsoft by six to 12 months, as the prospect of a heavily remote workforce for the foreseeable future now looks [on] the cards,” he wrote, as reported by MarketWatch.

Keith Weiss, an analyst at Morgan Stanley, is also bullish on the stock. He reiterated an overweight rating, raising the price target from $198 to $230, according to The Fly. Weiss said that although IT budgets have been contracting marginally, Microsoft has clearly benefited from companies who are prioritising virtual collaboration and cloud computing.

Going into fiscal 2021, even if the company were to miss the Q4 2020 earnings guidance, things do look positive for Microsoft’s share price. Microsoft’s greater focus on hardware, software and services over advertising revenues may prove to be its biggest advantage over other big tech stocks.

Of 33 analysts polled by CNN, 29 rate Microsoft’s share price a buy, two outperform and three hold.

Source: This content has been produced by Opto trading intelligence for Century Financial and was originally published on cmcmarkets.com/en-gb/opto

Disclaimer: Past performance is not a reliable indicator of future results.

The material (whether or not it states any opinions) is for general information purposes only and does not take into account your personal circumstances or objectives. Nothing in this material is (or should be considered to be) financial, investment or other advice on which reliance should be placed. No opinion given in the material constitutes a recommendation by Century Financial or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person.

Century Financial does not endorse or offer opinion on the trading strategies used by the author. Their trading strategies do not guarantee any return and Century Financial shall not be held responsible for any loss that you may incur, either directly or indirectly, arising from any investment based on any information contained herein.

Regulated by SCA

Century Financial Consultancy LLC

Reach us:

-

Dubai

6th Floor, Emaar Square Building 4,

Downtown, Dubai, P.O. Box 65777,

Dubai, United Arab Emirates -

Abu Dhabi

27th Floor, Office 2701,

Shining Towers, Abu Dhabi, UAE - +971 (4) 356 2800

- info@century.ae

Disclaimer: Trading in financial products carries substantial risk. Leveraged over-the-counter (OTC) derivatives, such as Contracts for Difference (CFDs) and spot forex, may result in losses exceeding initial deposits and may not be suitable for all investors. These complex instruments do not confer ownership of the underlying assets. Investors should carefully consider their investment objectives and risk appetite, and seek independent professional advice if necessary.

Century Financial Consultancy LLC (CFC) is licensed and regulated by the Securities and Commodities Authority (SCA) of the UAE under license numbers 20200000028 and 301044 to carry out the activities of Trading Broker in international markets, Trading Broker of OTC derivatives and currencies in the spot market, Introduction, Financial Consultations, and Promotion. CFC is incorporated under UAE law, registered with the Dubai Economic Department (No. 768189), with its office at 601, Level 6, Building No. 4, Emaar Square, Downtown Dubai, UAE, PO Box 65777.

The content on this website is provided solely for informational and educational purposes and does not constitute an offer, recommendation, or solicitation to buy or sell any securities or financial products.

Products and services offered by CFC are not intended for use in any jurisdiction where such use or distribution would breach local laws or regulatory requirements.

Alert: Fraudulent Activity Notice

Century Financial Consultancy LLC (“Century”) has become aware of fraudulent individuals and entities impersonating our firm through unofficial websites, social media channels, and messaging applications such as Telegram, WhatsApp, and Discord.

Please be advised:

- Century does not manage investments on behalf of clients.

- Century does not solicit funds or guarantee investment returns.

- Century does not accept or make payments in cash, cryptocurrency, or digital assets.

- We do not conduct business via social media or messaging platforms.

Our only official website is www.century.ae, and all communication is conducted exclusively through verified channels.

We strongly urge the public to remain vigilant, verify the authenticity of any communication claiming to be from Century, and report any suspicious activity. Century disclaims any responsibility for losses arising from dealings with unauthorised or fraudulent parties.